As I write virtually every year at this time, I cannot predict the future, nor do I think ANYONE else can. While the Mary Meekers, Elon Musks, Bill Gateses, etc., will often come up with insights of how the economy and world will evolve, if you review their predictions you will find they are wrong as often as they are correct.

December, however, is a useful time to reflect on the key trends from 2018 that are likely to extend into 2019, impacting opportunities for those in the mobile and gaming space.

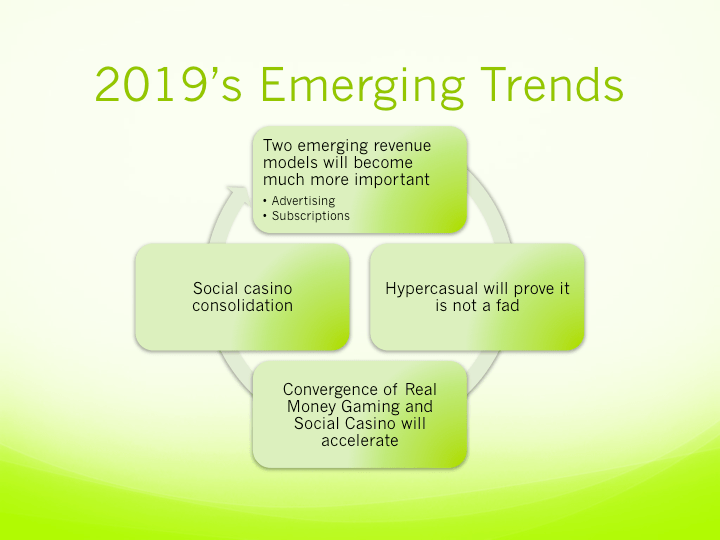

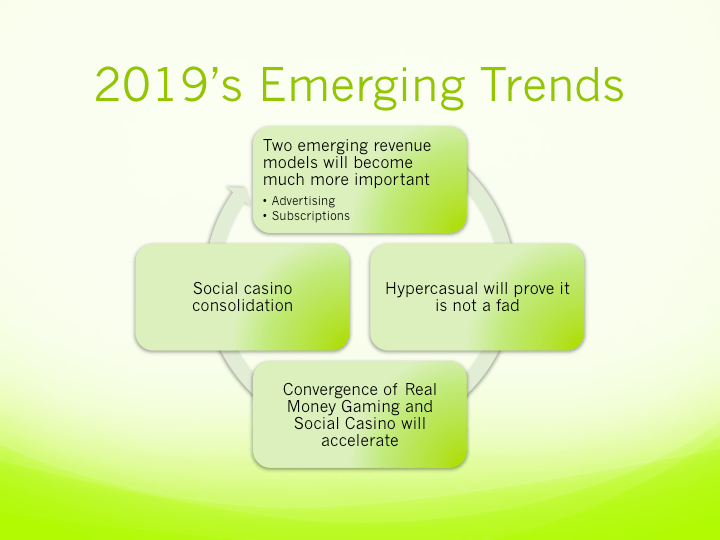

Two emerging revenue models will become much more important

While in-app purchases (IAP)will continue to drive revenue for social casino and social games, two other revenue sources will grow in importance.

- Advertising revenue.While advertising revenue already been the primary revenue source for many social games, it still represents only a small percentage of total social game revenue and many applications. In 2019, I expect advertising to become more important for all apps, particularly social casino. If done correctly, watch to earn videos do not cannibalize IAP revenue from spenders and creates revenue from the 95+ percent who do not monetize. Not only do ads not cannibalize IAP revenue, it often increases it by improving engagement and retention.

Additionally, as customer growth in many social gaming verticals stagnates, particularly social casino, it will be increasingly important to generate additional revenue from existing players. Advertising will provide incremental revenue that complements the other product initiatives and allows companies to cast a wider net in their user acquisition activities.

- Subscriptions become another revenue option. While advertising will grow as a revenue source for social casino and social games, subscriptions will make an even greater impact. The subscription model has worked very well in Asia, it is a large part Tencent is valued at over $350 billion, but has not made a big difference in the mobile gaming space in the west (US and Europe). It is also the key to Netflix’s success and arguably Amazon’s (see Amazon Prime). Mobile game companies are finally understanding how to incorporate subscriptions in their business models, rather than just throwing them out there as an additional in-app purchase. The strength of subscriptions throughout the economy suggest it can become as important or even more important than IAPs eventually for social games.

Hypercasual will prove it is not a fad

The biggest development in social gaming in 2018 was the rise of hypercasual games, which now make up more than 50 percent of all mobile downloads. They have also dominated the M&A scene, with Zynga buying Gram Games for $250 million, Goldman Sachs investing $200 million in Voodoo as well as multiple smaller deals. Hypercasual games typically have a single mechanic and a single goal, yet reaching a high score can be very difficult. Effectively the core game loop is very straightforward, do one thing, get rewarded (so you can try again) and keep repeating to get a higher score.

In 2019, I expect the hypercasual segment to mature. By mature, I do not see lower growth but a more professional approach. Companies will no longer succeed by throwing a lot of products at the market. Instead, the industry will fragment, with different companies focusing on specific demographics or gameplay mechanics. I also expect you will see higher product values, while a $25k hypercasual game can be a huge success now, competition will raise the bar. UIUX will improve as will technical stability (today’s hypercasual games remind me of Facebook games from 2012, while games crashing are part of the experience). The increase in quality will eventually drive out the small and independent developers (except for the best and the brightest) but will result in better consumer experiences.

Convergence of Real Money Gaming and Social Casino will accelerate

With both Real Money gaming and social casino becoming increasingly competitive, they will lean more heavily on each other to capture best practices and improve their businesses. Social casinos are great at progression and social mechanics and these features will increasingly find their way into real money gaming, where just adding games no longer will be enough for success. On the social side, with the ability to grow the social slots market seemingly coming to an end, social casinos will take more gaming mechanics (sports betting, live dealer, virtual sports) from real money and adapt them to the social space.

Also, real money online gaming companies will get over their phobia that social gaming is cannibalistic and realize what their land based brethren discovered years ago, the two businesses are complimentary and increase the size of the pie. Social gaming provides the trigger for players to want to play roulette or slots and can also prove a great brand building opportunity. Partnerships similar to MGM’s relationship with Play Studios (where MyVegas and Play Studio’s other games share MGM’s rewards program) will extend into the real money space. As the US real money market emerges, real money operators will be increasingly anxious to partner with social casino companies to access their players.

Social casino consolidation

With user growth slowing in the social casino space, the top companies have to look elsewhere to grow their businesses. They have proven quite adept at increasing revenue from existing users, leading to unbroken annual growth for the past ten years that is likely to continue for at least another few years. But growing revenue per user has its limits, and the owners of the top social casino companies are demanding even more growth. While companies have had mixed (i.e. disappointing) results purchasing small players, the major casinos are driving growth by acquiring the other big boys. Late 2017, Aristocrat purchased Big Fish for about $1 billion. DoubleU also acquired DoubleDown Casino for over $800 million. These two deals have created the number 2 and number 3 social casino companies and I expect this trend to accelerate in 2019 as there will be limited other options for rapid growth.

Return to blogging

One prediction I can be 100 percent confident in is that I will be blogging more in 2019. While the real world got in the way of my blogging in 2018, there are many topics I plan to cover in 2019. I also look forward to any ideas from my friends and followers on topics you would like to see me discuss.

Retrospective

It would be intellectually dishonest if I wrote about my expectations for 2019 without reviewing how my picks for 2018 did. So how did I do last year:

- The convergence of micro-segmentation, AI and machine learning to create extreme personalization. In 2018, the social casino industry continued to experience strong growth despite flat user numbers. The key driver for this growth has been better personalization and segmentation, the successful companies are tailoring promotions and sales for individual users. If anything, I expect this trend to accelerate in 2019 as companies actually understand what they are doing with machine learning and AI.

- Voice recognition. While it has not had a big impact on the social casino space, voice driven devices continue to gain ground with Google and Apple joining Amazon promoting voice heavily. I expect in 2019 game companies will figure out how to combine the growth of voice with gaming products.

- Big change in social casino. I will call this one a slight miss as the space has not evolved dramatically. Stars Group did release the first social casino games, PokerStars Play and Jackpot Poker, with Live Dealer but overall the industry did not change much from 2017. I still expect an innovative company will change the market in 2019.

- Devices and platforms will become less important. I will admit to a miss here, the ecosystem still revolves around Apple and Google.

- Dual devices. Another slight miss here. Dual devices have become a reality but they have not significantly impacted the game space.

- Big players will enter free to play, and fail. This was a big miss and indicative of a sea change but one I am very happy about. After years of social casino and mobile gaming overall being the shiny thing and companies make stupid investments to get into the space, the business has rationalized. Companies are now looking at the competitive situation and financials before moving into the space, leading to a much more rational environment.

- Privacy. BOOM, did I get this one correct. As someone who personally does not worry too much about my online privacy, privacy became the story of 2018. While privacy concerns will not go away in 2019, I think the concerns will ebb as people understand how to control what they share. The days of aggressively compiling and sharing user data, however, are gone and those companies that still act in a rogue way put their whole business at risk.

See you in 2019, have a great year.

Key takeaways

- 2019 should see the emergence of two additional revenue streams for social casino and social games, subscriptions and advertising.

- Hypercasual will prove to have legs, remaining a dominant genre in gaming

- Real money gaming will borrow more from social casino in 2019 while social casino operators will try game mechanics popular in real money.