After spending three days at ICE, the largest B2B iGaming show in the world, I wanted to share some of the highlights. While there was nothing dramatically different this year, it reinforced several trends:

There are many red oceans

I have written many times about blue oceans and red oceans, the former being spaces in the market where your competitors are irrelevant, the latter where you are competing directly with others. In the iGaming space, there is very little creativity and almost all the companies are just trying to be a little better than their competitors. There are a few silos in the industry, and within each silo the companies are largely interchangeable. Virtually all the companies, large and small, are imitating each other and adding minor twists around the fringes. The concern with this situation is that in a red ocean it is very challenging to maintain your margins and generate long-term growth.

Content as a commodity

The iGaming industry is evolving to a position where content is becoming a commodity, in part driven by the red ocean mentality. Technology and globalization is also contributing to this situation, as the barriers to entry are exceedingly low for content development. A good artist and designer anywhere — Chicago, Bangalore, Vilnius or Jakarta — can create a beautiful slot. While math is critical, there are many great mathematicians who can make the beautiful slot into a decent game. Not only does good content flood the market, it allows operators to create their own content cost effectively and skim a large part of their revenue into machines that do not generate third party royalties.

While this problem runs counter to the concept that content is king, content is not king if it is virtually the same. Content that stands out still enjoys premium pricing and attracts more players and operators. Great content cannot be replaced with quickly made internal product. Very little content, though, falls into this bucket and most is competing for an increasingly small revenue pool.

While this situation is bad news for content creators, it is great for operators. The plethora of slot providers puts the basic supply and demand formula in favor of operators. They can negotiate more favorable royalty deals or build their own competitive machines with minimal cost.

Platforms offering zero value

Consistent with the glut of content is a glut of platforms and aggregators. In the video game space, there are many “publishers” who will license a game, take a share (sometimes very significant) and just submit the game to the AppStores, adding virtually zero value.

In the iGaming space, many people have created platforms where they aggregate slots content and distribute it to operators. The problem is that many of these platforms or aggregators have few relationships with operators, and even the operators who have integrated them put the content in the back of the virtual store. There were many stories at ICE of slots developers who have generated dollars or only cents from an integration with a platform. Just as in the video gaming space, content providers need to do their due diligence before selecting a platform.

Lots of people speaking American

For many years, G2E has been the gambling show that Americans went to while ICE was largely for Europeans, but I heard many American accents this year. Additionally, some traditionally US focused companies — Everi, AGS, Scientific Games, etc. — had large presences at ICE. It shows the US companies, particularly content providers, understand that the online real money market (which is dominated by Europeans) dwarfs the US land based market. Europe provides a great opportunity for many of these companies, though it also means more content on the market.

Not everyone got the memo about crypto

While the bloom is off the crypto rose almost everywhere, particularly tech, many iGaming companies are still operating on the momentum it had twelve months ago. Throw the word crypto on a mediocre offering and expect it to be worth an order of magnitude more. This approach is consistent with how the industry reacts and copies rather than seeks blue oceans, so I am confident that next year there will be very little crypto left and they will be chasing the next one year old trend.

The promise of virtual sports

Not all the news is bad. The quality and breadth of the virtual sports offerings is very impressive. Walking through the virtuals area was like being at a sports bar with multiple TVs showing live events. The rendered virtual sports are often better than games available for console, like Madden or FIFA. There are also some great offerings that put together video clips of live events and create a virtual event. I expect virtual sports to be a big growth area online (both real money and social) in the next few years.

Key takeaways

At ICE this year, there was little new and many companies copying each other, competing in a red ocean.

There is a glut of slots content, driving down revenue for slots providers but potentially providing a cost savings for operators.

Virtual sports represents the best opportunity for growth, as the quality of the content is improving exponentially.

When I listed my expectations for 2019, the one that generated the most conversation was that the convergence between Real Money Gaming and social casino would accelerate. The underlying driver of this convergence is that both ecosystems are strong and have many learnings to offer. Real Money casino is a $10.6 billion business. Meanwhile, social casino is a $5.4 billion industry that has grown every year since 2012 and is projected to continue growing 7-12 percent per year through 2022.

What social casino can learn from Real Money gaming

Content is king

Real Money casinos focus on adding more content (slots and table games) to increase revenue. While social casino operators also will profess content is king and acknowledge that new games are the strongest driver of KPIs, they do not have the singular focus on adding content that their Real Money counterparts have. Most social casino companies are happy releasing a new slot every second week and launching with 20-30 machines. Conversely, the top Real Money casinos often have over 500 slots and introduce new games much more rapidly.

Given the proven results from launching new content, social casinos should look at much more aggressive content schedules. To achieve this result, social casinos will need to move from their reliance on exclusive, homemade content.

Real Money operators can launch hundreds of games because they license the slots non-exclusively, thus providing access to thousands of slot machines and table games. While exclusivity does provide a unique selling point, many of the homemade social slots are not truly unique. They have common themes and standard math, they are effectively a commodity. Thus the exclusivity is only a perceived advantage, it has no value to the player. Rather than recreating the wheel for every machine, social casinos can still create a unique machine every two weeks (or four weeks or one week) but supplement it with non-exclusive content from the many third-party slot developers.

Cross-sell

While most social casino operators are focused on creating a strong slots app and then optimizing acquisition for that app, Real Money operators have a more robust model. While they still will acquire slots players for their casino products, they have entire verticals that exist largely to acquire players that can be cross-sold into casino. Virtually all the Real Money Bingo products derive the bulk of their revenue from slots. While sports betting is a profitable real money vertical on its own, all of the major sports betting companies rely on slots to drive LTV and allow for more aggressive user acquisition.

In the social space, the siloes are much stronger. Only Kama Games, which uses products like Blackjackist and Roulettist to drive traffic to its poker offering, regularly uses other casino mechanics to acquire players and then cross sell them to its core poker product. Even the social game companies with strong bingo products generally treat bingo as a standalone vertical with its own P&L, just acquiring players for bingo rather than to cross sell into their slots offerings.

Social game companies need to look more at their ecosystem rather than individual products. This will allow them to acquire more players at a higher ROI.

New mechanics

All successful social casino products are based on mechanics proven in the real money space (either land based or online) but not all real money gaming mechanics have made it to social casino. One of the challenges faced by social casino is that the number of players is no longer growing. While revenue continues to increase, it is driven by better monetization of the player base, rather than expanding the player base. One of the most obvious ways to appeal to more players is offering more gameplay options.

There are several real money mechanics that could benefit social casino companies:

Sports betting. Sports betting is the largest Real Money gaming vertical, worth well over $22 billion. Social casino companies have tried to replicate Real Money sports betting apps with no success; they have failed for several reasons. The products are normally very complicated, not lending itself to a new sports betting player. Sports betting is also very event driven (you are only interested when there is a match you want to bet on), while social games rely on strong daily retention. Despite these issues, given the overall interest in sports, strength of social fantasy applications and lack of Real Money sports betting in some core markets, a creative game designer can come up with the killer social app for this segment.

Virtual sports. Virtual sports is an important but small part of the online real money gaming ecosystem. Technology, however, has made it much more viable and a great option for social casino companies. Virtual sports are similar to slot machines in that winning is based on a random number generator with set odds, they just simulate a real sporting event. Technology, however, has made these simulated games look as good as real sports. The video below from virtual sports provider Inspired Gaming shows these matches look better than what you would see on a gaming console. Unlike actual sports betting, virtual sports are always available to the player so you can create an experience players can return to daily.

Live dealer. Live dealer games are the fastest growing mechanic in the real money gaming space. Companies led by Evolution Gaming, provide games where customers play against a live dealer or host through a video feed. Just as with virtual sports, technology has made this offering much better than only a few years ago, with smoother and higher quality streaming. It is the fastest growing segment of real money gaming and virtually when any B2C company reports its financial results, Live Dealer is the highlight or only bright spot. There are challenges integrating it into social games, bandwidth costs, one-to-one dealer requirements, etc., but as Stars Group showed these issues can be overcome.

New Audience

Real Money gaming shows that the addressable market is not limited to 40+ women. While 73 percent of social casino players are female, 65 percent of real money gamers (and 55 percent of real money casino players) are men. With user growth stagnant in social casino, appealing to a male demographic can expand the market for social casino.

Offer driven user acquisition

While social casino companies are more sophisticated with their overall digital marketing, Real Money operators are better at using promotional offers to bring in players. Promotions, such as a free money welcome bonus, spin to win, triple winnings their first day playing, etc., have a very strong pull. While the cost in Real Money of these promotions is sometimes challenging, in social casino they are less risky as providers are only gifting virtual currency. These offers are complicated by AppStore restrictions but this challenge is not insurmountable and more creative offers will improve social game companies user acquisition efforts.

VIP 3.0

While social casino is more reliant on VIPs than Real Money casinos, more than 60 percent of social casino revenue comes from 0.5 percent of players, Real Money operators are much more sophisticated in working with their VIPs. Only a few social casino operators, such as Zynga, have true VIP management programs, most social casinos have one person (who may also be responsible for social media or support) who runs their VIP “program.” Conversely, the most successful real money casinos have a more robust VIP support initiative:

Proactive. While much of VIP management in social casino is better customer support for spenders, VIP management in Real Money gaming consists of proactively reaching out to your top players and understanding them as a process. The VIP team can then anticipate problems or opportunities and provide a better experience to the player.

Rake back or loss return. Many real money gaming companies (both land based and online) refund part of player losses to their best players. This practice allows players to take more risks and helps overcome periods of bad luck. While it is a controversial practice, many in the real money space lament the cost is not worth the effort, it is a strong way to increase loyalty of your most active players.

First class promotions. Why are most fights in Las Vegas, answer is so the casinos can give their VIPs front row seats. Real Money operators will send their top players to great sporting events, sold out concerts, the top restaurants or even a luxury cruise to show their appreciation. While VIPs will often spend over $200,000 in a social game, these VIPs are often rewarded with a t-shirt (if they are lucky). Treating top VIPs similarly to the real money industry will keep them more engaged with social casino offerings.

Hospitality events. Not only do Real Money casinos send their VIPs to great events, they create great events. By creating your own event, you are building something unique that competitors cannot replicate and the player cannot get anywhere else. Thus, they are less likely to churn as they would not want to lose access to these events, while they can always buy fight or concert tickets. It is also a great opportunity for your VIP team to build personal relationships with your VIPs, and the personal bond is often stronger than financial benefits of being a VIP.

By replicating these practices, social casinos can reduce VIP churn and improve their lifetime value to the company.

What Real Money gaming can learn from social casino

Although Real Money casino is a larger business, in many ways it is less sophisticated than social gaming. For many years, Real Money casino operators could succeed by getting a stable product in front of customers. With LTVs upward of $400, they had significant margin of error in user acquisition and product features. Conversely, social casinos continuously had to optimize all facets of their business to continue growing. This optimization has led to the development of many features and tactics that can benefit Real Money gaming.

Progression

Providing progression serves many valuable purposes in games. First, it gives people a reason to play, they want to keep moving forward. Even in Real Money gaming, studies have shown over 65 percent do not play to win money, thus progression will appeal to the majority of these customers.

Progression also prevents churn. Loss aversion is a very strong driver of behaviour, people do not want to lose something they already have. The endowment effect also explains that they will also overvalue it.

In addition to reducing churn, progression increases engagement. Players want to complete as many levels as quickly as possible. If there are outstanding levels, they will want to reach them as they will want to finish everything open.

Progression also is a strong monetization driver. Candy Crush is a great example of a game genre that did not monetize but by adding progression King.com was able to create a billion-dollar franchise. Progression prompts players to want to keep playing even when they are out of chips, so thus depositing more, and to play at higher stakes, increasing their bet size.

In the Real Money casino world, where players will often jump between casino offerings to capitalize on the best promotions, progression creates loyal and valuable customers.

Social features

Social features are another strong behaviour driver that has largely been perfected by free to play games. Social interaction is a core value for customers, driving success across many industries. While many features satisfy base needs, social interaction appeals to a higher need and thus people are willing to pay more for it and less likely to give it up. The success of Big Fish Casino, and more recently Huuuge Games, shows how social features can create a unique and very profitable market position. Outside of the casino space, Clash of Clans is a great example of social features driving billions in revenue.

There are many different types of social features that Real Money casino operators can implement, with some of the most successful including:

Guilds or clans, where players join together to overcome challenges or compete with other groups.

Group challenges, so players have to team together to win rewards.

Chat, to enable players to interact with each other.

Customizable and useful player profiles, so players can know more about other players.

Social shares to unlock gifts.

Personalized videos, so players can share their gameplay with friends.

Team competitions, where players form teams to get higher scores (which could be chips won) than other teams.

Synchronous slot game play.

Social lobby, so players know they are not playing alone.

Visibility into where friends and other players are winning.

Player review of games and slots, similar to Amazon.

Referral program, so your players can also be your evangelists.

Some of these features will work better in certain products than others but a mix of these features will not only create bonds with your players but amongst your players.

UIUX

Social casino developers provide a much cleaner and smoother user interface (UI) and user experience (UX) than real money gaming companies. Players can quickly start playing and there is virtually no learning curve. It is easy to navigate in the product, take advantage of offers and understand every offering. Real Money, conversely, often overwhelms the customer with choice, increasing the cognitive load. This problem is not only in the lobby but in the products, betting options are often very complex and confusing. Overall, social gaming companies create an experience much more consistent with customers expectations in 2019.

In-product VIP

While Real Money gaming companies are great at hosting and managing their VIPs, social game companies are much better at giving them incentives and rewards in product. Virtually all social casinos have an in-game VIP system, where the more VIPs play, the more privileges they earn. This type of automated system provides continuous reinforcement and reminds VIPs why they want to remain in their favourite product.

Events

Within the past year, social casinos have become very adept at creating events that boost engagement. It could be the December Challenge or the Race to the Mountain Top, but in effect it is a collection of challenges and specialized content that is available for a limited time. Often the player has a chance to win an item(s) that is only available by completing the event and will not be available again, creating an incentive both to participate and to visit the game regularly (so they know about the events). These events also break the monotony of playing the same games repeatedly. Finally, they can provide an incentive to try new slots or mechanics.

The most successful social games are now running at least one event daily and this practice can be replicated in the Real Money world. A regular schedule of events increase loyalty, engagement and monetization.

Key takeaways

The strength of both the Real Money Gaming and social casino businesses suggest they both have many lessons to offer.

Social casino companies should focus on adding even more content than they do currently (in part by using third party content they do not have exclusively), create an ecosystem based on cross-sell, try game mechanics from Real Money gaming (sports, virtual sports, live dealer), try to engage male players, create more unique new player offers and replicate the high-touch VIP programs found in real money.

Real Money casinos can improve their profitability by adding progression mechanic, social features, more simple user interface and user experience, in-product VIP programmes and daily events.

As I write virtually every year at this time, I cannot predict the future, nor do I think ANYONE else can. While the Mary Meekers, Elon Musks, Bill Gateses, etc., will often come up with insights of how the economy and world will evolve, if you review their predictions you will find they are wrong as often as they are correct.

December, however, is a useful time to reflect on the key trends from 2018 that are likely to extend into 2019, impacting opportunities for those in the mobile and gaming space.

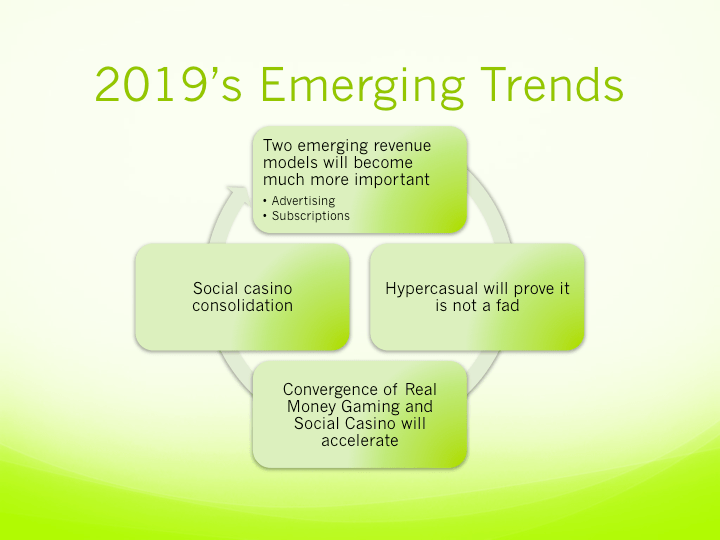

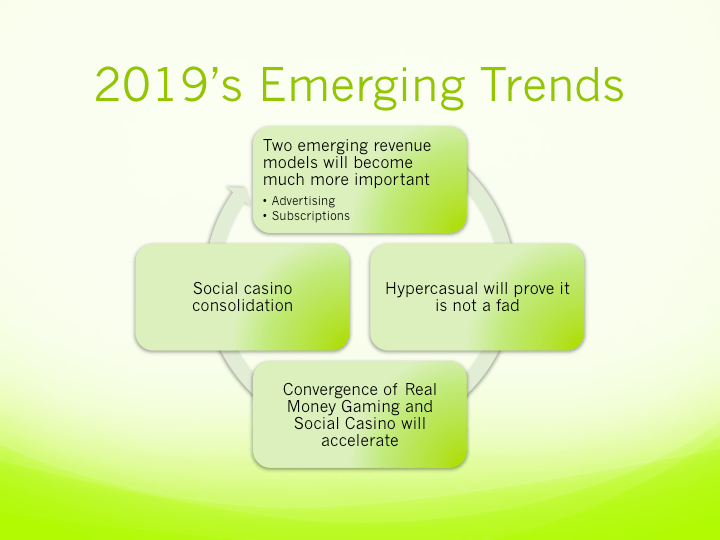

Two emerging revenue models will become much more important

While in-app purchases (IAP)will continue to drive revenue for social casino and social games, two other revenue sources will grow in importance.

Advertising revenue.While advertising revenue already been the primary revenue source for many social games, it still represents only a small percentage of total social game revenue and many applications. In 2019, I expect advertising to become more important for all apps, particularly social casino. If done correctly, watch to earn videos do not cannibalize IAP revenue from spenders and creates revenue from the 95+ percent who do not monetize. Not only do ads not cannibalize IAP revenue, it often increases it by improving engagement and retention.

Additionally, as customer growth in many social gaming verticals stagnates, particularly social casino, it will be increasingly important to generate additional revenue from existing players. Advertising will provide incremental revenue that complements the other product initiatives and allows companies to cast a wider net in their user acquisition activities.

Subscriptions become another revenue option. While advertising will grow as a revenue source for social casino and social games, subscriptions will make an even greater impact. The subscription model has worked very well in Asia, it is a large part Tencent is valued at over $350 billion, but has not made a big difference in the mobile gaming space in the west (US and Europe). It is also the key to Netflix’s success and arguably Amazon’s (see Amazon Prime). Mobile game companies are finally understanding how to incorporate subscriptions in their business models, rather than just throwing them out there as an additional in-app purchase. The strength of subscriptions throughout the economy suggest it can become as important or even more important than IAPs eventually for social games.

Hypercasual will prove it is not a fad

The biggest development in social gaming in 2018 was the rise of hypercasual games, which now make up more than 50 percent of all mobile downloads. They have also dominated the M&A scene, with Zynga buying Gram Games for $250 million, Goldman Sachs investing $200 million in Voodoo as well as multiple smaller deals. Hypercasual games typically have a single mechanic and a single goal, yet reaching a high score can be very difficult. Effectively the core game loop is very straightforward, do one thing, get rewarded (so you can try again) and keep repeating to get a higher score.

In 2019, I expect the hypercasual segment to mature. By mature, I do not see lower growth but a more professional approach. Companies will no longer succeed by throwing a lot of products at the market. Instead, the industry will fragment, with different companies focusing on specific demographics or gameplay mechanics. I also expect you will see higher product values, while a $25k hypercasual game can be a huge success now, competition will raise the bar. UIUX will improve as will technical stability (today’s hypercasual games remind me of Facebook games from 2012, while games crashing are part of the experience). The increase in quality will eventually drive out the small and independent developers (except for the best and the brightest) but will result in better consumer experiences.

Convergence of Real Money Gaming and Social Casino will accelerate

With both Real Money gaming and social casino becoming increasingly competitive, they will lean more heavily on each other to capture best practices and improve their businesses. Social casinos are great at progression and social mechanics and these features will increasingly find their way into real money gaming, where just adding games no longer will be enough for success. On the social side, with the ability to grow the social slots market seemingly coming to an end, social casinos will take more gaming mechanics (sports betting, live dealer, virtual sports) from real money and adapt them to the social space.

Also, real money online gaming companies will get over their phobia that social gaming is cannibalistic and realize what their land based brethren discovered years ago, the two businesses are complimentary and increase the size of the pie. Social gaming provides the trigger for players to want to play roulette or slots and can also prove a great brand building opportunity. Partnerships similar to MGM’s relationship with Play Studios (where MyVegas and Play Studio’s other games share MGM’s rewards program) will extend into the real money space. As the US real money market emerges, real money operators will be increasingly anxious to partner with social casino companies to access their players.

Social casino consolidation

With user growth slowing in the social casino space, the top companies have to look elsewhere to grow their businesses. They have proven quite adept at increasing revenue from existing users, leading to unbroken annual growth for the past ten years that is likely to continue for at least another few years. But growing revenue per user has its limits, and the owners of the top social casino companies are demanding even more growth. While companies have had mixed (i.e. disappointing) results purchasing small players, the major casinos are driving growth by acquiring the other big boys. Late 2017, Aristocrat purchased Big Fish for about $1 billion. DoubleU also acquired DoubleDown Casino for over $800 million. These two deals have created the number 2 and number 3 social casino companies and I expect this trend to accelerate in 2019 as there will be limited other options for rapid growth.

Return to blogging

One prediction I can be 100 percent confident in is that I will be blogging more in 2019. While the real world got in the way of my blogging in 2018, there are many topics I plan to cover in 2019. I also look forward to any ideas from my friends and followers on topics you would like to see me discuss.

Retrospective

It would be intellectually dishonest if I wrote about my expectations for 2019 without reviewing how my picks for 2018 did. So how did I do last year:

The convergence of micro-segmentation, AI and machine learning to create extreme personalization. In 2018, the social casino industry continued to experience strong growth despite flat user numbers. The key driver for this growth has been better personalization and segmentation, the successful companies are tailoring promotions and sales for individual users. If anything, I expect this trend to accelerate in 2019 as companies actually understand what they are doing with machine learning and AI.

Voice recognition. While it has not had a big impact on the social casino space, voice driven devices continue to gain ground with Google and Apple joining Amazon promoting voice heavily. I expect in 2019 game companies will figure out how to combine the growth of voice with gaming products.

Devices and platforms will become less important. I will admit to a miss here, the ecosystem still revolves around Apple and Google.

Dual devices. Another slight miss here. Dual devices have become a reality but they have not significantly impacted the game space.

Big players will enter free to play, and fail. This was a big miss and indicative of a sea change but one I am very happy about. After years of social casino and mobile gaming overall being the shiny thing and companies make stupid investments to get into the space, the business has rationalized. Companies are now looking at the competitive situation and financials before moving into the space, leading to a much more rational environment.

Privacy. BOOM, did I get this one correct. As someone who personally does not worry too much about my online privacy, privacy became the story of 2018. While privacy concerns will not go away in 2019, I think the concerns will ebb as people understand how to control what they share. The days of aggressively compiling and sharing user data, however, are gone and those companies that still act in a rogue way put their whole business at risk.

See you in 2019, have a great year.

Key takeaways

2019 should see the emergence of two additional revenue streams for social casino and social games, subscriptions and advertising.

Hypercasual will prove to have legs, remaining a dominant genre in gaming

Real money gaming will borrow more from social casino in 2019 while social casino operators will try game mechanics popular in real money.