I am speaking at the PDMA Inspire Innovation conference later this month if any of you are attending. I would love to meet up and happy if you joined my talk: Digital Product Development Strategy: Maximizing Success Through Strategic Prioritization.

I am speaking at the PDMA Inspire Innovation conference later this month if any of you are attending. I would love to meet up and happy if you joined my talk: Digital Product Development Strategy: Maximizing Success Through Strategic Prioritization.

I have started converting my favorite posts from this blog to Podcasts, using a text to voice engine. You can access the podcasts on multiple sites if you prefer to listen:

Happy holidays to everyone and I hope you all have a wonderful New Year! Please come back for new posts in 2018, I am looking forward to writing about some interesting topics. Have a great holiday season!

I have always been interested in decision making and how people often are not logical in not only their preferences but even how they remember and look at facts. The most useful book I ever read was Thinking, Fast and Slow by Daniel Kahneman, (highly recommend it if you haven’t read it yet) and one of my favorite academics is behavioral economist Dan Ariely. Not only does Kahneman and Ariely’s research help you understand consumer behavior, it helps you understand your own decision making and, most importantly, mistakes most of us make.

A recent guest blog post on the Amplitude Blog, 5 Cognitive Biases Ruining Your Growth, does a great job of describing five biases that can greatly impact your business. While I will try to avoid just repeating the blog post, below are the five biases and some ways they may be impacting you:

A product manager may have driven a new feature, maybe a new price point on the pay wall. Rather than running an AB test (maybe insufficient traffic or other changes going on), they then review the feature pre and post launch. Game revenue per user increased 10 percent so they create a Powerpoint and email the CEO that there new feature had a 10 percent impact. Then the company adds this feature to all its games. The reality is that at the same time the feature was released the marketing team stopped a television campaign that was attracting poorly monetizing players. The latter is actually what caused the change in revenue. As someone who has known a lot of product managers, I can confirm this bias in the real world.

Two branded games are in the top 5 of new releases. All of the analysis is that branded games are now what customers are looking for. The realities is that the two games, totally unrelated, had strong mechanics and were just that lucky 10% of games that succeed. Allowing the Narrative Fallacy to win, however, you then put your resources to branded games, which are no more popular than before the launch of the two successful titles.

Again, for the example from the game industry. Let’s say you want to port your game to a new VR platform. You go to your development team and they say it won’t be a problem. You sign up for the project, give them the specs, six months later they still cannot get the game to run on the VR platform as they have no idea how to develop VR (this is a nicer example than some others I can remember).

As an example, you decide to analyze how your company has been calculating LTV. You look back at the analysis done the last two years and see how actual LTV tracked with projections at that time. You discover that you underestimated actual spend by 50 percent. Should be great news, will allow you to ramp up dramatically your user acquisition. Instead, when you present this data to your analytics team, they refuse to accept it, saying your analysis is flawed because you are not looking at the right cohorts.

Given that I want to keep this blog post under 500 GB, I will not list all the examples of the bandwagon effect I have seen in the game industry. Product strategy, however, is the most obvious culprit. When the free to play game industry started to evolve to mobile, everyone started porting its Facebook games over to mobile. Since Zynga and the other big companies were doing it, all of the smaller companies as well as newly funded ones also tried to bring the same core mechanics from Facebook over to mobile. Mechanics that worked on Facebook, however, did not work on mobile but companies continued doing it because everyone else was. Rather than identify the market need and a potential blue ocean, companies just joined the bandwagon.

The key to making the right decisions is not to assume you do not have biases, but always to be diligent in reviewing your decisions and making sure you are thinking rationally. All of these biases can lead to personal or company failure, so the inability to identify them can have extreme consequences.

Businesses always have had to deal with external risk (as opposed to business risk, ie. a competitor bringing out a better product) but it seems that these risks are magnified in the current environment where we are seeing seismic and often unexpected changes in government, economic policies, etc. Were automakers who moved operations to Mexico prepared for a Trump victory, were banks who set up international headquarters in London thinking about Brexit, were call centers that built their infrastructure in Manila ready for Duterte? The same goes for legislation and regulatory, were companies that based their operations in Ireland expecting the Google ruling or were trucking companies ready for the cap on greenhouse emissions?

Many companies take the position that they cannot control or predict these risks so they just need to conduct business as usual and deal with situations when they occur. That attitude, however, can leave you company with few or no options and thus unable to recover from the external shock.

Fortunately, risk is not new and over the years the companies that have best sustained success have developed ways of dealing with risk. I came across an article from 2009 in the McKinsey Quarterly, Risk: Seeing Around The Corners by Eric Lamarre and Martin Pergler, that shows best practices in identifying (and thus preparing for) potential risks.

Most companies do have some system in place to identify risk, though I have seen some whose systems is bury your head in the sand, but even with systems in place they often only look at direct risk. For example, they may be worried about the risk of being banned from China so the government can help a local company, but they are not looking at the risk that a drought in China could bankrupt all their local distributors.

Lamarre and Pergler point to the situation in Canada in 2007 when the Canadian dollar appreciated 30 percent versus the US dollar. The Canadian manufacturers did understand the impact of the currency change on how competitive they were in the US. Most Canadian companies, however, did not see how it would impact Canadian consumers (75% of whom live within 100 miles of the US). Thus, not only did their US sales crater but so did the bulk of their Canadian sales. They actually had hedged to minimize the impact on US sales, but they were unprepared (and many did not have the resources) to protect themselves from the squeeze on revenue in Canada.

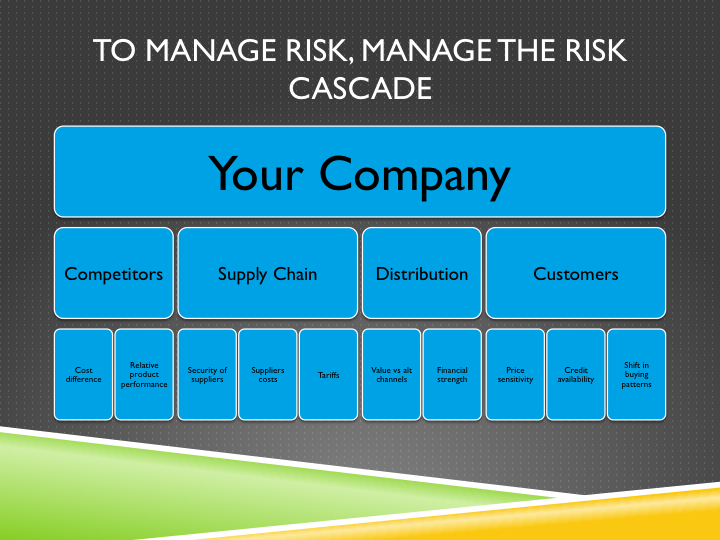

The best way to assess and manage risk is to look at all levels of the value chain. Once you understand these risk areas, you can see how they cascade to the core competitiveness of your business and what steps you need to take to mitigate the risk. The key areas of the value chain to analyze are competition, supply chain, distribution and customers.

While most companies constantly monitor their competitors’ product offerings, the greatest risks are often less obvious. External factors might change a company’s cost position versus its competitors or substitute products. Companies are particularly vulnerable to this type of risk cascade when their currency exposures, supply bases, or cost structures differ from those of their rivals. Sometimes good and sometimes bad but all differences in business models create the potential for a competitive risk exposure.

For example, look at two fast food hamburger chains. The fast food business is largely price/value dependent. If one year a drought drives up the price of livestock feed, which then drives up the price of beef by 50 percent, it could have a huge impact on a company that sells millions of hamburgers. It should not fundamentally change the business because all chains face the same situation. However, if your competitor regularly hedges the price of beef by buying futures, then they can potentially keep prices constant even if beef prices spike while you might have to increase substantially your price. Thus a previously stable economic situation could quickly change to one where you can no longer compete. If some players hedge and others do not, cattle price increases force the nonhedgers to take a significant hit in margins or market share while the hedgers make windfall profits.

Companies must often extend the competitive analysis to substitute products or services, since a change in the market environment can make them either more or less attractive. In the hamburger example, high cattle prices indirectly heighten the appeal of salads, which would drive down demand for burgers.

The goal is not to mimic your competitors to eliminate these but think about the risks you implicitly assume when your strategy departs from theirs.

Supply chain risk often cascades to your business. If you are a technology company and cloud storage costs double overnight (maybe due to new regulations), all the software as a service companies that were giving you services would be forced to increase their prices. While you may have created contingencies yourself to manage your cloud storage costs, you probably would not have anticipated the cost increases of all SAAS suppliers. If some of your competitors managed these services internally, they may not have to shift their prices or service significantly. Thus, it is not only the direct impact of the change in costs but also the indirect impact.

Indirect risks can also lurk in distribution channels: typical cascading effects may include an inability to reach end customers, changed distribution costs, or even radically redefined business models. Facebook is a great example of this risk in two ways. When it first embraced gaming, it provided some companies at that time (i.e. Zynga, Playdom and Playfish) a way to reach hundreds of millions of people at very little cost. Thus traditional game companies like THQ and Acclaim saw their share of users wallets decrease or have their players pulled away to the Farmvilles and Social Cities of the time. So even though FB did not directly impact THQ and Acclaim, it effectively bankrupted them.

Then, when Facebook changed its model in 2011 so companies had to pay it 30 percent of revenue, the impact both direct and indirect had a huge competitive impact. Overnight, profitability for FB dependent game companies fell 30 percent, forcing companies to change their cost structure, migrate to other channels or cease to exist. Companies that were not dependent on Facebook, primarily other online MMO companies, had a significant advantage. While social game companies may have been aware of the risk of Facebook credits, they generally did not understand how it would benefit certain competitors.

The most difficult risk to anticipate are the responses from customers, because those responses may be so diverse and so many factors are involved. One typical cascading effect is a shift in buying patterns, with consumers using another distribution channel. As Lamarre and Pergler write, “another is changed demand levels, such as the impact of higher fuel prices on the auto market: as the price of gasoline increased in recent years, there was a clear shift from large sport utility vehicles to compact cars, with hybrids rapidly becoming serious contenders. Consider too how the current recession has shrunk the available customer pool in many product categories: demand for durable goods plummeted among consumers holding subprime mortgages as their access to credit shrank, and demand for certain luxury goods fell as even financially stable consumers turned away from conspicuous consumption.”

The key to anticipating risk and managing your exposure is to assess the full risk cascade. Exploring how that risk propagates through the value chain (competitors, supply chain, distribution and customer response) can help you think through what might change fundamentally when some element in the business environment does.

To manage the risk cascade properly, there are several steps:

In these volatile times, it is important to anticipate and have contingencies for external events that can significantly impact your business. Simply saying who could expect a certain election result or a natural disaster and thus our company is bankrupt is not an excuse except possibly in your next job interview. Good companies will be ready to not only deal with but also capitalize on external changes that they do not control.

For those planning or considering attending EiG (Excellence in iGaming) in Berlin next month, I will be part of a very interesting panel on that Tuesday, the 18th of October. Paul Lucey (Twitter’s Head of Gaming for EMEA), Amar Kumra (Google’s Industry Manager – Social Gaming) and I will be discussing how you can appeal to the next generation of gamers. I am actually very excited to hear what Paul and Amar have to say and it should be a great discussion. If you will be in Berlin, let me know and we can meet up.

I am looking to fill two positions on my Free-to-Play team at PokerStars. We are currently ramping up our existing offerings (multiple apps with over 400,000 DAU) and have some exciting plans for next year. It is also a great opportunity to work on the Isle of Man, one of the most beautiful and safest places in the world and gateway to Europe.

The first position is Head of Free-to-Play CRM and VIP Strategy. This person will refine and finalize our CRM strategy as well as hire and build a VIP concierge team and social media marketing team. For those who read this blog regularly, you know how about CRM and VIP are to me.

The second position is a Product Manager focused on monetization. I like to describe this position as the Janet Yellen of PokerStars Free-to-Play.

If you or any colleagues are interested in either of these positions, I encourage you to apply or email me directly.

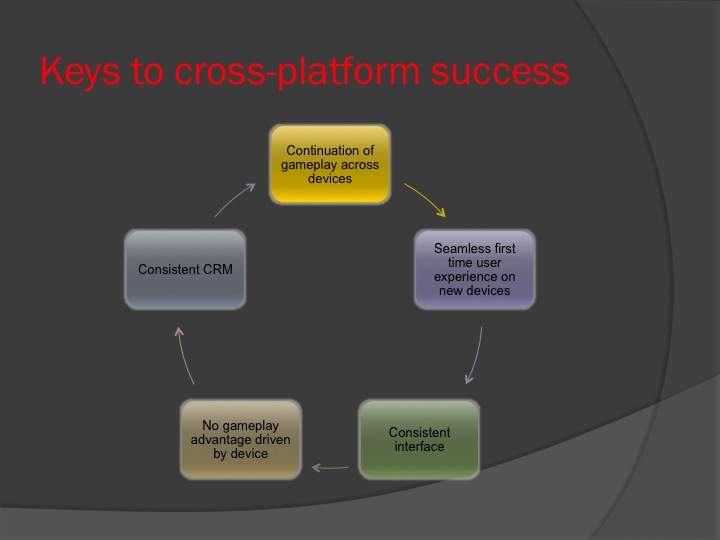

While most game companies talk cross-platform, they really mean putting their product on multiple platforms rather than optimizing play for customers who want to play on different devices at different times. They are missing an important opportunity, or alienating their users, by not focusing more effort on creating a great experience across platforms. I came across an article on Adweek’s SocialTimes, Study: Customers (Especially Millenials) Hate When You Fail To Deliver Cross-Platform Experiences, that provided great data on what happens when you do not have a good cross-platform user journey.

More than half users switch devices mid-activity. The number is highest for Millennials, where 90 percent switch devices mid-activity. With GenXers, it falls to 76 percent and with those 55 or older, it is 58 percent. What is striking in these numbers is that even with the lowest number, more than 50 percent still switch devices mid-activity.

When it comes to playing games, the number falls but is still quite significant. 14 percent of all US customers change devices mid-activity. 25 percent of US Millennials change devices mid-activity while playing games.

You thus need to craft messaging that is relevant for a player or user who started on one device and is now playing your game or shopping on your site on a different device. The article quotes an Adobe analyst as saying, “that means digital marketers have a unique challenge of being able to really understand that a Web visitor who shows up on a smartphone is the same customer four hours later on a tablet, or seven hours later on a desktop. They have to piece that experience together in order to craft a consistent message to that one consumer, regardless of which device they use.”

While many games now allow you to share your balance across devices, there is an opportunity to please better your players be integrating further. There are several steps a game company can make to create a great cross-device experience.

I have written many times about satisfying your customer and catering to their multi-device activity is one of these instances. If you do not create a great experience, a competitor will and you will start losing players. Moreover, these are probably your most engaged customers, so the cost of replacing them is even greater.

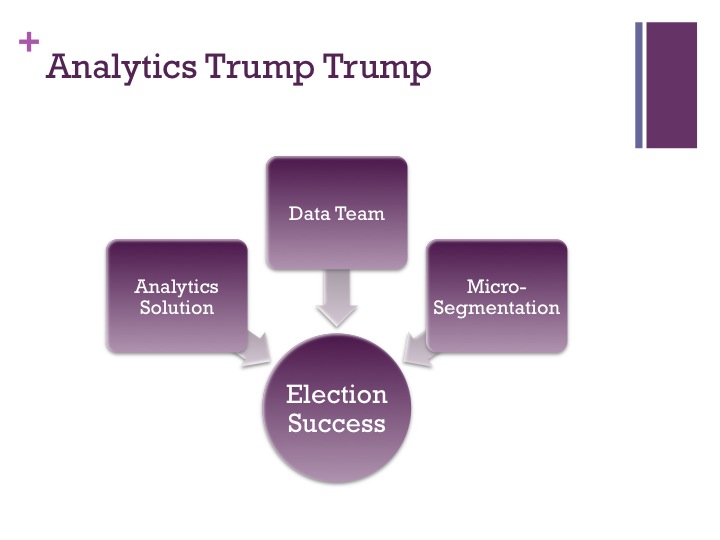

There is a great article on Politico, How Trump Let Himself Get Out-Organized, that explains how Trump’s Iowa debacle was a result of a failed analytics strategy. Trump made the same mistake many companies commit, he felt a strong brand and what he believe compelling product allowed him to under-invest in analytics. This issue was compounded by the aggressive use of analytics by competitors. Although this occurred in the political arena, there are lessons for all businesses.

The article explains that despite Trump’s strength in the polls, he did not have “the tools they needed, which is why they overpromised and underperformed.”

While Ted Cruz and Marco Rubio spent millions building sophisticated voter targeting machines, Trump did not start building a data operation to target voters until mid-October. It did not even start buying data (i.e. voter lists, etc) until November and waited to December to start using the Republican National Committee’s (RNC’s) voter file.

The Trump campaign declined to use Cambridge Analytica, a behavioral modeling company with political expertise, due to cost. Cruz, however, retained Cambridge Analytica’s services and the firm is now widely credited with engineering Cruz’s cutting-edge targeting operation. Rubio, who also over delivered on expectations, spent $750,000 for an outside company to assist in its data operations. Trump overall spent $560,000 on data services in 2015, compared to $3.6 million by the Cruz campaign. It is also about $700,000 less than Trump spent on hats.

The Iowa caucas also showed the value of having a strong analytics team, not simply software. Cruz’s data team, which they call the Oorlog (the Afrikaner word for ‘war’) project, includes four full-time data scientists and embedded talent from Cambridge Analytics.

The Rubio campaign, which also exceeded expectations, has also invested heavily in its analytics team. It has a 22-person data war room in DC.

The Cruz campaign also hired ten canvassers (and recruited many volunteers) to go door-to-door to contact people the analytics suggested were supportive or could be persuaded. Traditionally, these so-called match rate initiatives are 50 percent successful but with Cruz’s advanced analytics the success rate reached 70 percent. The Cruz campaign also used the voter profiles to shape its strategies for most marketing activities, from television ad buys to telephone banks.

Micro-segmentation, or creating very small customer segments and treating them uniquely, is another area where Trump fell down compared to Cruz. As Politico wrote, the Cruz campaign, “built a list of more than 9,000 Iowans who were still on the fence between their candidate and Trump. The team divided the undecided voters ― who were heavily evangelical and 91 percent male ― into more than 150 different subgroups based off ideology, religion and personality type, Wilson said. It used Facebook experiments to determine which issues jazzed up their voters the most.”

No matter how strong you feel your product is, or how well it has performed in the past, you are vulnerable to competitors who may have a superior analytics solution. To combat this risk, you not only need to match the investment your competitor’s are making in analytics and look at micro-segmentation but also build a world class data team.

I hope everyone has a wonderful holiday and fantastic New Year! See you all next year.