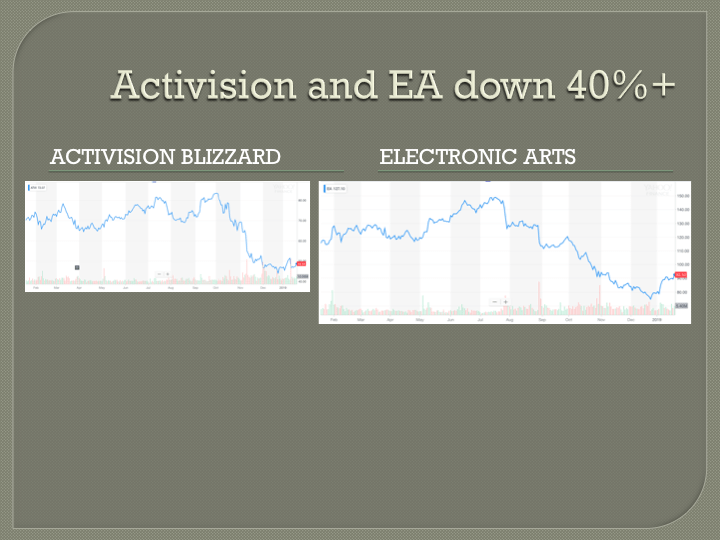

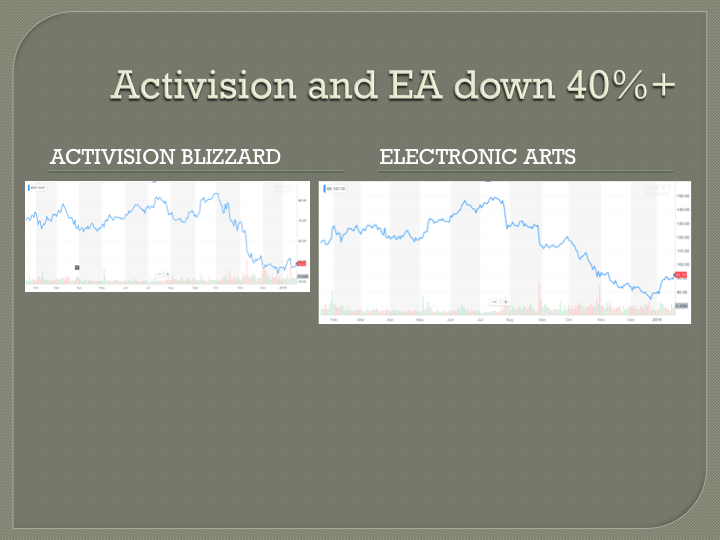

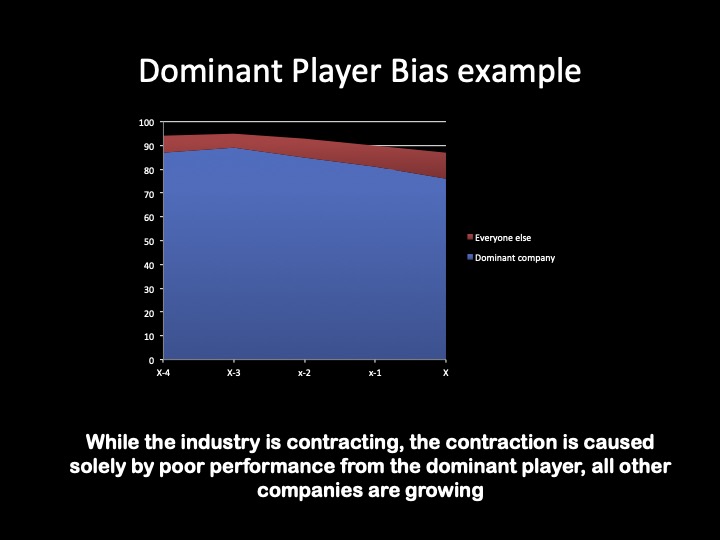

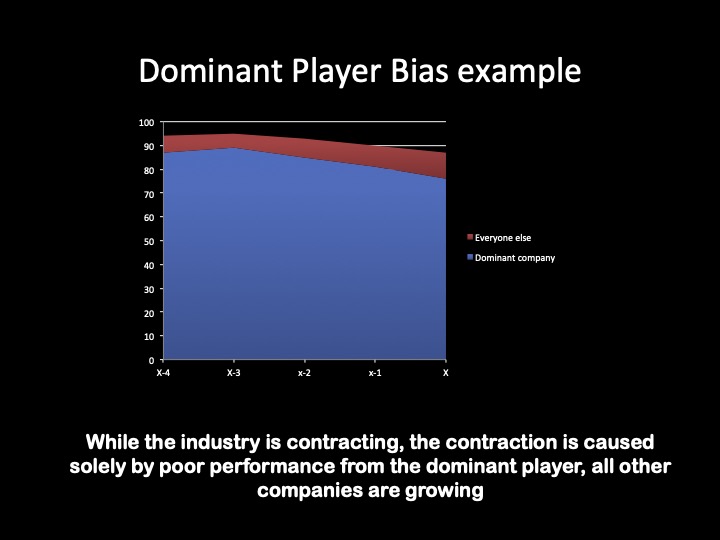

One cognitive bias that is often overlooked is equating the performance of an industry or sector with that of its dominant player. When one company represents 60, 70, 80+ percent of a market, its fortunes will drive the growth (or decline) rate of the industry. This growth, however, may be due to mistakes or issues with the dominant company rather than the underlying market and potential of the space. This bias, what I refer to as Dominant Player Bias, risks abstaining from good business opportunities and misallocating resources, missing Blue Oceans and accepting sub-optimal performance. The chart below shows how one company’s poor performance can imply the entire sector is contracting, though the problems are due to the dominant company rather than reduced interest:

There are many examples where the fortunes of the dominant company are equated with the fortunes of the industry. Facebook has nearly 70 percent of the social media market and if people lose interest in Facebook, it drives a decline in social media usage. Roughly, a 20 percent drop by Facebook, would drive down overall social media numbers about percent 15 percent (I am not using real numbers for the purpose of this example). Thus, investors may invest less in social media or other companies may accept declining usage because they feel the industry is contracting significantly. The actual cause though may be Facebook’s customers’ dissatisfaction with privacy or advertising policies. Dominant player bias has caused these investors and competitors to equate Facebook’s performance with the social media landscape.

There are several actual examples of dominant player bias (the Facebook one above is for illustrative purposes only). When Zynga’s performance dropped significantly after its IPO in 2011, many heralded the end of social gaming. The success (and valuation) of companies like King.com, Epic, Supercell, etc., show that the underlying market remained healthy and Zynga was performing due to internal issues (shift to mobile, reliance on the Facebook feed, etc.).

Underestimating the market

The first problem caused by Dominant Player Bias is that it prompts companies to underestimate, and thus under-invest, in a market. To use the Facebook example, if Facebook is facing difficulties but people misinterpret its problems for shrinking demand for social media, they are underestimating the market and thus missing potential opportunities. These opportunities include:

- The dominant player under-investing and seeking to diversify. If they do not realize that internal decisions have led to falling performance, they may seek to diversify or even exist a market with high potential because they believe the potential market is smaller than it actually is

- Competitors may shy away from trying to build a business in the market because they feel it is not worth the investment. This bias can result in under-investment in new product development, marketing or other avenues that companies could challenge the dominant player. In this case, dominant player bias is actually compounding the problem because if the market is shrinking due to poor performance by the dominant player, it is actually a great opportunity for someone else to come in and try to break its hold on the market.

- Investors are less likely to fund companies with ideas that can disrupt the market if they perceive the sector is not attractive. Investors might underestimate the potential of an opportunity if they think the market is shrinking, though the market may only be shrinking because of poor decisions by the dominant player.

While dominant player bias can be either positive or negative, it is not a significant problem when it exaggerates the market potential. If a great company is continually expanding the market, then the great company’s performance is a good proxy for the overall opportunity.

You may miss a Blue Ocean

Another issue generated by Dominant Player Bias is that it might blind companies or investors to Blue Ocean opportunities. I have written several times about Blue Ocean strategy, rather than competing directly find an adjacent market space where there is no competition, and how Blue Oceans over time generate a higher return than competing in red oceans. If you succumb to Dominant Player Bias, however, you may never find the Blue Ocean because you falsely decide it is not worth looking for. This problem is particularly salient in industries with a dominant player, because their dominance may have prevented them from appealing to anyone except their existing customers (who they feel represent the entire market).

A great example of Dominant Player Bias and how a Blue Ocean strategy proved it wrong is the circus industry. Years ago, Ringling Brothers dominated the market. However, they let their product get stale and did not react well to changing tastes. Most observers at the time, 1984, believed that the overall circus market was dying and not worthy of investment. The founders of Cirque de Soleil, however, saw past this bias and realized it was the Ringling Brothers offering, not the circus market, that was causing the decline and launched a reimagined product. Now Cirque de Soleil is orders of magnitude larger than Ringling Brothers ever was because the Cirque founders were not convinced the circus market was dying due to Ringling’s poor performance.

A convenient excuse

Whether you are the major company or one of the small players, dominant player bias can mask under-performance, and thus opportunities to improve your company. Rather than looking inwardly, either intentionally or unintentionally, poorly performing dominant companies will blame the market for poor results. This bias will lead to several problems:

- Resources are under-allocated to the market where they have a dominant position. As mentioned earlier, dominant companies normally enjoy higher profit margins. Rather than trying to grow these businesses further (and thus increase a high margin business), internal investment is diverted to other efforts that have a lower ROI because the market potential of the core market is underestimated.

- There is unnecessary diversification or divestment. If the company believes the market it dominates is declining due to existential issues, it may diversify or close its business in the sector while it could enjoy a higher return if it resolved the internal problems leading to declining results.

- The dominant player misses opportunities to expand the market because they misinterpret declining results for a smaller market.

- Allowing poorly performing leaders to remain in critical positions. Rather than realizing deficiencies in leaders, poor results are blamed on overall conditions. This mistake keeps weak leaders in place rather than in competitive markets where the strongest leaders rise to the top and help improve the company’s fortunes.

Concentration is often the cause of an industry’s decline

While most companies dream of dominating their market, the type of concentration that creates Dominant Player Bias also can negatively impact the dominant player. By not facing competition, the company is not forced to innovate or grow the market. Instead, it enjoys monopoly rents, and thus a high profit margin, but is not focused on creating additional value. Without a focus on improvement, these companies usually reach a peak where they consider their huge market share the ceiling.

They do not provide anything to people who might not like their product but would enjoy something somewhat different. They also suffer from the innovator’s dilemma, they are satisfying existing who they know very well but because of their focus on their customers they do not create offerings that appeal outside the existing market. Over time, because others experience Dominant Player Bias, nobody brings new products to market, and the perception that the market is saturated leads to the reality that there are no new customers. Additionally, when a company enjoys a dominant position, the cost to them of acquiring new customers is very high relative to the value (almost everyone knows the dominant player, the low- and mid-hanging fruit has already been picked, etc.) so resources are focused on increasing profitability, generally by cutting costs. Since there is no effective competition, in the short term the company sees higher profits but eventually people are driven to alternatives (there are always alternatives, just potentially not direct alternatives), which creates a declining market (though the market shrinking is not driven by a smaller addressable market but by the dominant player reducing the total net value it is providing). This decreasing market both negatively impacts the dominant player over the long-term and prompts other companies to avoid entering the space.

The antidote for dominant player bias

To counter Dominant Player Bias everyone (the dominant player, competitors, potential market entrants, investors, etc.) should focus on the underlying market dynamics and the value to the customer rather than the short or mid term trends in the market. Going back to the Zynga example, looking in the mirror it is clear how other companies avoided Dominant Player Bias. If rather than looking at Zynga’s troubles and extrapolating it to the social gaming market, you looked at the value they were giving game players with a product that appealed to an untapped market (non-core gamers) and a business model (free-to-play) that made it easy for consumer to test and enjoy products, you would have seen that there was still a tremendous opportunity. That is exactly what happened at King and Supercell and Scopely, who avoided Dominant Player Bias and built billion dollar companies. By focusing on how much value you can deliver, it is much easier to scope the market rather than relying on how much one company has already delivered.

Key takeways

- Dominant Player Bias is when you mistakenly think a sector is contracting because the dominant firm is performing poorly, while the underlying cause is mistakes by the dominant firm.

- Dominant Player Bias impacts both the dominant company and competitors (and potential competitors), as it prompts them to underinvest in the sector and not seek new, Blue Ocean, ways to expand the market.

- To combat Dominant Player Bias, you should look at the underlying value to customers and potential customers, rather than the performance of one company.