Key takeaways

- We operate in a very volatile environment worldwide, with many external risks (Brexit, Trump’s victory, Russia’s invasion of Ukraine) difficult to predict but very impactful.

- To succeed, you not only should look at direct risks but overall risks to the value chain that will cascade to your company.

- The key is to understand and plan for risks that will impact competitors, your supply chain (anything from raw materials to cloud capacity),distribution channels and customers. Good companies will be ready to not only deal with but also capitalize on external changes that they do not control.

Dealing with risk

Businesses always have had to deal with external risk (as opposed to business risk, ie. a competitor bringing out a better product) but it seems that these risks are magnified in the current environment where we are seeing seismic and often unexpected changes in government, economic policies, etc. Were automakers who moved operations to Mexico prepared for a Trump victory, were banks who set up international headquarters in London thinking about Brexit, were call centers that built their infrastructure in Manila ready for Duterte? The same goes for legislation and regulatory, were companies that based their operations in Ireland expecting the Google ruling or were trucking companies ready for the cap on greenhouse emissions?

Many companies take the position that they cannot control or predict these risks so they just need to conduct business as usual and deal with situations when they occur. That attitude, however, can leave you company with few or no options and thus unable to recover from the external shock.

Fortunately, risk is not new and over the years the companies that have best sustained success have developed ways of dealing with risk. I came across an article from 2009 in the McKinsey Quarterly, Risk: Seeing Around The Corners by Eric Lamarre and Martin Pergler, that shows best practices in identifying (and thus preparing for) potential risks.

Risk is not only direct risk

Most companies do have some system in place to identify risk, though I have seen some whose systems is bury your head in the sand, but even with systems in place they often only look at direct risk. For example, they may be worried about the risk of being banned from China so the government can help a local company, but they are not looking at the risk that a drought in China could bankrupt all their local distributors.

Lamarre and Pergler point to the situation in Canada in 2007 when the Canadian dollar appreciated 30 percent versus the US dollar. The Canadian manufacturers did understand the impact of the currency change on how competitive they were in the US. Most Canadian companies, however, did not see how it would impact Canadian consumers (75% of whom live within 100 miles of the US). Thus, not only did their US sales crater but so did the bulk of their Canadian sales. They actually had hedged to minimize the impact on US sales, but they were unprepared (and many did not have the resources) to protect themselves from the squeeze on revenue in Canada.

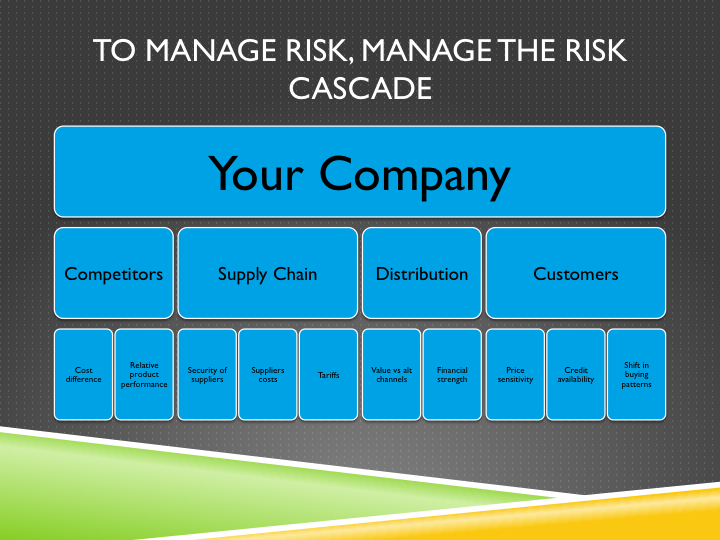

The best way to assess and manage risk is to look at all levels of the value chain. Once you understand these risk areas, you can see how they cascade to the core competitiveness of your business and what steps you need to take to mitigate the risk. The key areas of the value chain to analyze are competition, supply chain, distribution and customers.

Risk related to competition

While most companies constantly monitor their competitors’ product offerings, the greatest risks are often less obvious. External factors might change a company’s cost position versus its competitors or substitute products. Companies are particularly vulnerable to this type of risk cascade when their currency exposures, supply bases, or cost structures differ from those of their rivals. Sometimes good and sometimes bad but all differences in business models create the potential for a competitive risk exposure.

For example, look at two fast food hamburger chains. The fast food business is largely price/value dependent. If one year a drought drives up the price of livestock feed, which then drives up the price of beef by 50 percent, it could have a huge impact on a company that sells millions of hamburgers. It should not fundamentally change the business because all chains face the same situation. However, if your competitor regularly hedges the price of beef by buying futures, then they can potentially keep prices constant even if beef prices spike while you might have to increase substantially your price. Thus a previously stable economic situation could quickly change to one where you can no longer compete. If some players hedge and others do not, cattle price increases force the nonhedgers to take a significant hit in margins or market share while the hedgers make windfall profits.

Companies must often extend the competitive analysis to substitute products or services, since a change in the market environment can make them either more or less attractive. In the hamburger example, high cattle prices indirectly heighten the appeal of salads, which would drive down demand for burgers.

The goal is not to mimic your competitors to eliminate these but think about the risks you implicitly assume when your strategy departs from theirs.

Supply chains

Supply chain risk often cascades to your business. If you are a technology company and cloud storage costs double overnight (maybe due to new regulations), all the software as a service companies that were giving you services would be forced to increase their prices. While you may have created contingencies yourself to manage your cloud storage costs, you probably would not have anticipated the cost increases of all SAAS suppliers. If some of your competitors managed these services internally, they may not have to shift their prices or service significantly. Thus, it is not only the direct impact of the change in costs but also the indirect impact.

Distribution channels

Indirect risks can also lurk in distribution channels: typical cascading effects may include an inability to reach end customers, changed distribution costs, or even radically redefined business models. Facebook is a great example of this risk in two ways. When it first embraced gaming, it provided some companies at that time (i.e. Zynga, Playdom and Playfish) a way to reach hundreds of millions of people at very little cost. Thus traditional game companies like THQ and Acclaim saw their share of users wallets decrease or have their players pulled away to the Farmvilles and Social Cities of the time. So even though FB did not directly impact THQ and Acclaim, it effectively bankrupted them.

Then, when Facebook changed its model in 2011 so companies had to pay it 30 percent of revenue, the impact both direct and indirect had a huge competitive impact. Overnight, profitability for FB dependent game companies fell 30 percent, forcing companies to change their cost structure, migrate to other channels or cease to exist. Companies that were not dependent on Facebook, primarily other online MMO companies, had a significant advantage. While social game companies may have been aware of the risk of Facebook credits, they generally did not understand how it would benefit certain competitors.

Customer response

The most difficult risk to anticipate are the responses from customers, because those responses may be so diverse and so many factors are involved. One typical cascading effect is a shift in buying patterns, with consumers using another distribution channel. As Lamarre and Pergler write, “another is changed demand levels, such as the impact of higher fuel prices on the auto market: as the price of gasoline increased in recent years, there was a clear shift from large sport utility vehicles to compact cars, with hybrids rapidly becoming serious contenders. Consider too how the current recession has shrunk the available customer pool in many product categories: demand for durable goods plummeted among consumers holding subprime mortgages as their access to credit shrank, and demand for certain luxury goods fell as even financially stable consumers turned away from conspicuous consumption.”

How you should look at risk

The key to anticipating risk and managing your exposure is to assess the full risk cascade. Exploring how that risk propagates through the value chain (competitors, supply chain, distribution and customer response) can help you think through what might change fundamentally when some element in the business environment does.

To manage the risk cascade properly, there are several steps:

- Look at the direct risks and how they will impact your business.

- Take those same direct risks and see who they will impact your competitors, they the supply chain, then distribution and then your customers. For each of these, determine how that impact will effect your business.

- For each of the four elements of the value chain, look at their direct risks. Then look at how that risk will impact the other three elements on the value chain. From there, determine how it will impact your business on the value chain.For example, identify the risks to your customers. Maybe the value of their local currency will decrease due to changing political affiliations. With a weaker currency, they will have inflation and more of their wallet will go to core products. They will thus have less disposable income. For you, it may mean you are at a disadvantage to local suppliers (whose costs are in the local currency) or that these people will just be spending less on your product category. Thus, if you are well prepared, you may have a lower cost product available or be able to shift your marketing to territories where users are less impacted.

- Build contingency plans not only for the direct and obvious risks, but other risks that can indirectly have a significant impact on your business.

Managing risk is a central ingredient to your success

In these volatile times, it is important to anticipate and have contingencies for external events that can significantly impact your business. Simply saying who could expect a certain election result or a natural disaster and thus our company is bankrupt is not an excuse except possibly in your next job interview. Good companies will be ready to not only deal with but also capitalize on external changes that they do not control.