While revenue in the social casino space continues to increase (a streak that has not been broken since the first days of Zynga Poker and Slotomania), dark clouds on the horizon have started to dampen the enthusiasm. Most social casino companies would not publicly disclose that they are expecting growth to slow (or reverse) but unspoken indicators are bearish.

Stagnant player growth

The greatest threat to the social casino industry is that the user base is not growing. Over the past couple of years industry revenue has continued to increase but active players has remained virtually stagnant. The revenue growth has been driven by certain companies (particularly Playtika) becoming increasingly adept at growing revenue per customer, especially among their VIPs. At some point, however, social casino operators will hit a ceiling as VIPs cannot and will not spend more.

Actions show that the top companies do not believe in the space

While no social casino operator has publicly warned about the challenges they are facing, their actions speak more loudly. Playtika, the largest social casino company, acquired Seriously last month, after acquiring Wooga last year.

Huuuge Games, the biggest success story in the social casino space in the last three years, launched a publishing arm. Critically, it is focused on hypercasual and traditional social games (such as Traffic Puzzle) rather than social casino. Given how involved Huuuge is with social casino, if it expected tremendous growth it would almost certainly be focusing its efforts to further increase market share in this space.

The public markets are also talking

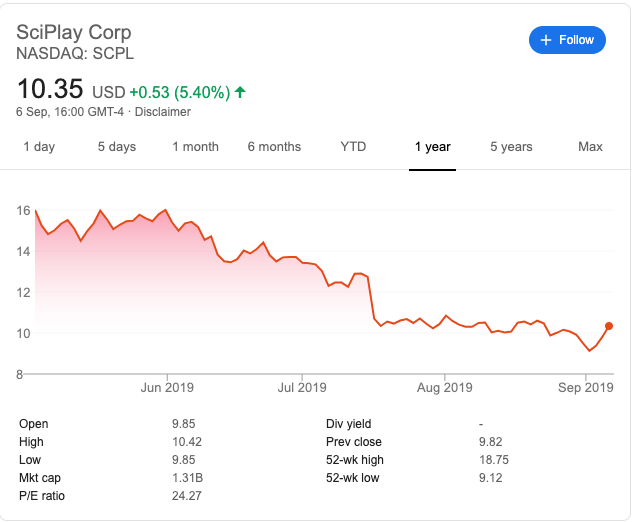

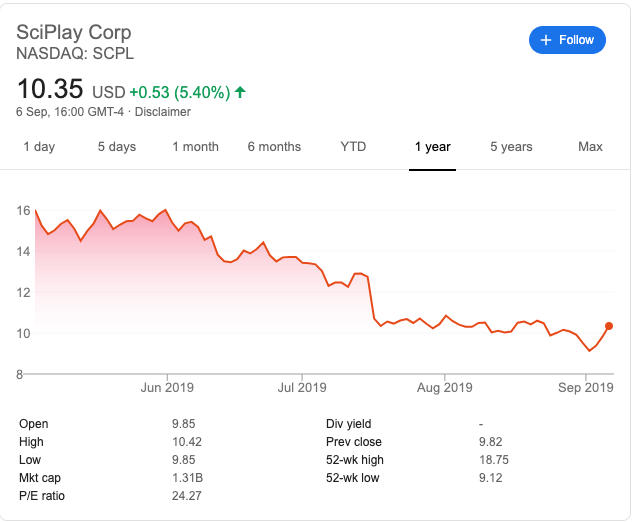

While social casino operators are showing how they look at the industry through their actions, the public markets also show how investors view the opportunities in social casino. The first pure play social casino IPO, SciPlay (the social casino operations of Scientific Gaming), has seen its share price drop from $16 when it went public in May to $10.35, losing over 30 percent of its value.

From 2015 to 2017, virtually every Zynga’s earnings call highlighted its social casino division. Initially, it focused on the growth of its slots products (primarily Hit It Rich!), which was largely the only bright spot for the company. Not only did it tout the success of its slots products, but the big IP licenses it was signing for future products (such as Willy Wonka). The calls then incorporated Zynga’s success with Poker, which experienced a renaissance. Very noticeably, over the last year, Zynga has downplayed or even ignored the role of social casino in its growth projections. In part, this is due to the success it has experienced with recent acquisitions (and the struggles it has experienced recently in the social casino space), but it also highlights that investors are not very receptive to initiatives in the social casino space.

Again, actions speak louder than words. While investors are not perfect (The Big Short, anyone), they are focused on optimizing return and look across a broad spectrum to find the best opportunities. The lack of appetite for social casino shows that investors no longer think social casino is easy money.

The other looming risk

Another cloud dampening the prospects for social casino is real money gaming. The US is disproportionally important for the social casino industry, it derives a much higher percentage of total revenue (over two thirds) than other areas of the video game industry (which derives over 50 percent of revenue outside the US). While there are too many factors to determine causality, the US is the only major social casino market where real money online casino is largely illegal. Thus, many customers who would normally play in a real money environment can only get their online casino experience through social casino.

Eventually, as real money casino play becomes legal in more US states, it represents an existential risk to the social casino industry. This risk is not an immediate one, legislation has to be approved on a state-by-state basis and I do not expect a significant number of states to approve legislation until 2022-2023 at the earliest (sports betting is a very different phenomenon). Investors and companies, however, do look beyond the next few years to determine their best opportunities and real money gaming is an acute part of that equation.

What social casino companies should do

First, innovate. While it sounds trite, innovation is the key to revitalizing the sector. The industry (and many other parts of the game industry) has been driven by copying what is already working, trying to do it a little better and continued optimization. They are thus relying on fewer players to generate more revenue. Coin Master is a great example of how a company can generate hundreds of millions of dollars in the social casino space by breaking the mold and creating a casino product for new customers. Finding Blue Ocean opportunities using casino mechanics can reverse the dynamics threatening the industry.

Second, embrace Real Money gaming. While Real Money is a risk, it is also potentially salvation. Land based casino companies largely resisted social casino for years (one particularly reactionary one still does) only to find that customers who also play social casino have a higher lifetime value. MGM’s relationship with Play Studios (MyVegas) has driven millions of dollars of value to MGM, displayed by MGM’s increasing its support (actions speak louder than words).

While the relationship between social and real money online has not yet been proven, the size of the opportunity should generate more attention from social casino operators. Real Money online gaming, a $54+ billion industry, dwarfs social casino. If social casino companies can learn how to capture a portion of that revenue (and player base), it can exceed greatly the growth rates of the past.

Key takeaways

-

- Despite growing every year since the first social casino products launched, the industry faces significant risks. There are highlighted by recent growth driven by improved monetization of existing players rather than appealing to new customers.

- Further corroborating this problem is how leading social casino companies are looking outside the space for acquisitions while investors are showing little interest in social casino.

- To combat these trends, social casino companies need to look for Blue Ocean opportunities (use social casino mechanics to appeal to new customers) and leverage the roll out of real money gaming.