I was fortunate recently to be invited to the Deconstructor of Fun podcast to talk with Joseph Kim and Brett Nowak (Founder/CEO of Liquid & Grit) about the future of the social casino space. For anyone interested in our conversation, listen to the Podcast or view the discussion on YouTube.

Category: Social Casino

Design + Behavioral Economics = Apple

I recently read a great book on Jony Ive (Jony Ive: The Genius Behind Apple’s Greatest Products by Leander Kahney), the designer who created most of Apple’s products, that provided insights into the keys to Apple’s success. What was particularly interesting is how much of his design philosophy was consistent with the behavioral economics and consumer behavior insights that I wrote about earlier this year after reading Rory Sutherland’s Alchemy.

Kahney’s book also showed that what many, including myself, considered good luck or timing by Apple were the result of decisions driven by Ive’s design philosophy. The iPod was not simply an MP3 player at the right time, the iPhone was not just another mobile phone that hit a nerve with customers and the iMac was not simply a pretty PC. These were all products driven by a fundamental design philosophy backed by consumer behavior principles.

While most people acknowledge Apple’s strengths, its success (one of the five largest companies in the world, valued at over $1 trillion) highlights how leveraging these principles builds value. It is impossible to replicate what Jobs and Ive did – just as an American football team cannot simply replicate what Belichek and Brady did – there are underlying principles that can help any company. These concepts are also extendable to other industries, including digital ones like iGaming and the video game sector.

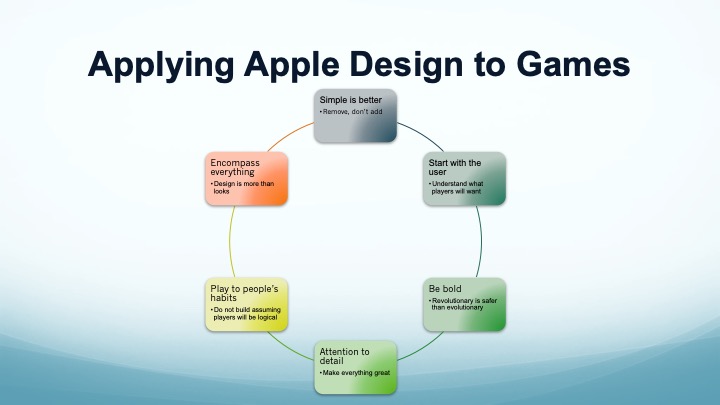

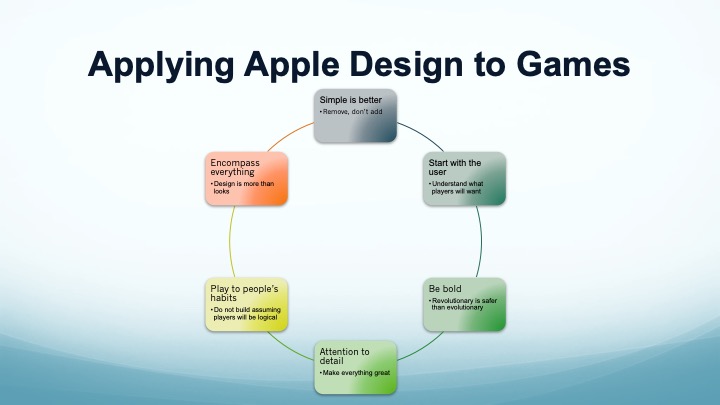

Simple is better

One of the key takeaways from Alchemy was that “Less is More”, a product with less functionality is more likely to change fundamentally behavior. This belief is also at the center of Ive’s design philosophy. Kahney writes about Ive, “the process of simplification is design 101, a mind-set that every design student is taught in school. But not every student adopts it, and it’s rarely applied with the ruthless discipline practiced by Jony…. The shy boy from Chingford is happiest when the user doesn’t notice his work at all.” Ive’s philosophy is also consistent with Job’s mantra: ‘Simplicity is the ultimate sophistication.’

This philosophy drove how Ive approached design. Not only did he aim for simple design, it was the centerpiece of how Apple built products. First, Ive did not focus on making his products pretty or cool; instead the focus was on simplicity. As Ive once said, “we are not interested in design statements. We do everything we can to simplify design.”

With Ive, simplicity was not limited to how a product looked. According to Kahney, “as part of his characteristic drive to reduce and simplify, Jony wanted to reduce the number of parts and therefore the number of part-to-part joints. Previously, when IDg [Apple’s internal design group] had done a similar dismantling of an original iPhone, the team counted nearly thirty interfaces where parts meet. After the iPhone underwent a unibody makeover, the number of interfaces shrank to just five.” Apple repeated this design principle over multiple products, from laptops (starting with the MacBook Air to phones to desktop computers). In all these cases, simplicity was much more than skin deep.

The story of the iPod is a great example of how an unwavering focus on simplicity led to incredible commercial success. Before reading Kahney’s book, I thought the iPod was a combination of good timing (music going digital), a beautiful looking design and integrated software (iTunes). The reality was that the iPod was a transformational product because of Ive’s and Job’s unwavering focus on simplicity.

The iPod was a result of Jony’s simplification philosophy. Kahney writes that “it could have been just another complex MP3 player, but instead he turned it into the iconic gadget that set the design cues for later mobile devices.”

What made the iPod successful was not cool new features but what it did not have. At the time, most electronic devices had removable batteries, meaning they needed a battery door, plus an internal wall to seal the device’s guts from the user when the battery door is opened. Jony dispensed with both, creating a tighter, smaller gadget. Ive also eliminated the on-off button, which infuriated many users (and reviewers). Instead he had the idea of pressing any button to turn the device on, and then to have it turn itself off after a period of inactivity, a stroke of minimalist genius.

On the software side, Apple acquired a third-party MP3 jukebox program for the Mac, SoundJam MP, from a small company, Casady & Greene. Apple then hired Casady & Greene’s top programmer, Jeff Robbin. Robbin’s team moved to Apple’s HQ and set about retooling SoundJam, stripping out many features to make it accessible to first-time users. Under the direction of Jobs, Robbin spent several months simplifying the program, which eventually turned into iTunes. The key to iTunes was what Robins removed from the program after it was acquired by Apple, not what features were added.

The iPod example not only shows the power of simplicity but also how hard it is. Getting rid of the on-off button took much more effort and time than simply redesigning or moving the button. Simplifying iTunes required the dedicated effort from one of the best developers in the world. What led to success, however, was Apple’s willingness to devote extraordinary resources to eliminating features and complexity rather than the natural tendency to put those resources into building more.

Play to people’s habits

A second takeaway, again consistent with Alchemy, is the importance of building something for how people behave, not just what they need. As Sutherland pointed out, not only is the logical and rational path not necessarily optimal, it is also not the one our customers might be pursuing. Before Apple, one of Ive’s biggest successes was designing the TX2 pen for a Japanese company. Jony’s innovation was to put something on a pen that was purely there to fiddle with. The pen’s design was not just about shape, but also there was an emotional side to it. The pen immediately became the owner’s prize possession, something people always wanted to play with. As Kahney writes, this “‘fiddle-factor’ notion may have seemed trivial to some, but the incorporation of the ball and clip transformed the pen into something special.”

Ive’s unusual pen anticipated built the kind of allegiance that later Ive-designed products at Apple would inspire. The handle on the iMac shows Ive’s understanding of non-traditional consumer behavior. It is not for carrying the iMac around, but to build a bond with the consumer by encouraging them to touch it. Kahney says, “it was an important but almost intangible innovation that would change the way people interacted with computers.”

Be bold

Another lesson in Apple’s success is to be bold. While people often feel it is less risky to iterate on proven design, the opposite is true. I once wrote it is less risky to pursue a Blue Ocean strategy than a Red Ocean one, as the latter places you in the middle of intense competition. In Alchemy, Sutherland also points out Logic does not necessarily lead to great, in many ways it drives you to average. The same is true of design, everyone is looking at making incremental improvements and your “new” design is likely to look like 20 of your competitors.

Ive and Jobs philosophy of simplification led to a need to make bold breaks from the past. The iMac was the first legacy-free computer. Apple ditched ADB, SCSI and serial ports, and included only Ethernet, infrared and USB. Apple also abandoned the floppy drive. These choices, particularly abandoning the floppy, generated intense criticism but were consistent with Ive’s and Job’s philosophy. If they were afraid of criticism, however, the iMac would not have disrupted the space.

Just as simplicity is not easy, neither is going legacy free when Apple designed the iPhone. Rather than improving on a Nokia or Motorola design, Ive and Jobs started from scratch. Kahney writes, “Apple attorney Harold McElhinny would describe the immense amount of work the project required. ‘It required an entirely new hardware system … It required an entirely new user interface and that interface had to become completely intuitive.’ He also said Apple took a huge leap of faith moving into a new product category. ‘Think about the risk. They were a successful computer company. They were a successful music company. And they were about to enter a field that was dominated by giants … Apple had absolutely no name in the [phone] field. No credibility….The arrival of the iPhone at Macworld was the culmination of more than two and half years of intense hardship, learning and dedication to bring it to market. As one Apple executive summed it up, ‘Everything was a struggle. Every. Single. Thing was a struggle for the entire two-and-a-half years.’”

Part of not just iterating involves focusing on the new experience, not other elements of the product. With the iPhone, Ivy and his team designed the phone without ever seeing the operating system. They initially worked with a blank screen and later, a picture of the interface with cryptic mock icons. Likewise, the software engineers never got to see the prototype hardware.

Start with the user

When applying behavioral economics, you learn that market research is often as unreliable as other data. As well as not always acting rationally, people often do not know what they prefer. Ive’s approach was consistent, as Kahney writes, “’we don’t do focus groups–that is the job of the designer,’ said Jony. ‘It’s unfair to ask people who don’t have a sense of the opportunities of tomorrow from the context of today to design.’….Jony was interested in getting things right and fit for a purpose. He was completely interested in humanizing technology.”

The iMac is a great example of this principle in practice. The machine did not revolve around chip speed or market share but Jony built it by focusing on how do people want to feel about it and what part of our minds should it occupy.

At Apple, designers focused on imagining objects that did not exist and bring them to life. Part of what they had to envision was defining the experience that a customer has when they touch and feel an Apple product, from the materials to the textures to the colors.

For Ive, the first step in creating a product was developing the design story. He did not feel he was building a product but instead was building the user’s perceptions and meaning of the product. According to Jon Fortt of the San Jose Mercury News, “Apple’s focus on the needs of the consumer made the iMac a hit. ‘What made the original iMac cool was not its color or shape. It was Apple’s demonstrated willingness to open the possibilities of Internet computing to an audience that had been ignored by the brainiacs who design PCs.’”

The focus was not on legacy but on the customer and how the user would feel about the device. Ivy once said, ‘when we are at these early stages in design, when we’re trying to establish some of the primary goals–often we’ll talk about the story for the product–we’re talking about perception. We’re talking about how you feel about the product, not in a physical sense, but in a perceptual sense.’

Attention to detail

Another key to Apple’s success is the attention to detail that Ive gave to design. His colleagues said, “whatever he did was never quite enough; he was always looking to improve the design….The level of finish was what was always amazing about his work relative to others. Others were and are capable of the conceptual thought and creativity but very few capable of that level of finish….The differences from one [of Ive’s] model to the next were subtle, but the step-by-step evolution betrayed Jony’s drive to thoroughly explore his ideas and get it right. Building scores of models and prototypes would become another trademark in his career at Apple.”

While many designers would focus on the visuals, Ive worried just as much about the guts of his designs. When people disassembled models he created, they found the inside of the models included the components. Ive had even worked out the thickness of the parts and how they would be manufactured in an injection moulder. Thus, when his designs moved to production, Apple could fulfill the vision without having to modify them to work.

The importance of attention to detail is reflected in how Jobs and Ive responded to impending bankruptcy. As Kahney quotes an Apple employee at the time, “you would have thought that, when what stands between you and bankruptcy is some money, your focus would be on making some money, but that was not [Steve Jobs’s] preoccupation. His observation was that the products weren’t good enough and his resolve was, ‘We need to make better products.’” The focus on making the perfect product is what Apple rode from near bankruptcy to near world domination.

Needs to encompass everything

Related to the focus on attention to detail was a focus on design encompassing everything, not simply the visual. I was amazed that Ive’s high-powered design team (and Jobs) would put the same effort in a product’s packaging as the actual product. Kahney writes, “boxes may seem trivial, but Jony’s team felt that unpacking a product greatly influenced the all-important first impressions. ‘Steve and I spend a lot of time on the packaging,’ Jony said then. ‘I love the process of unpacking something. You design a ritual of unpacking to make the product feel special. Packaging can be theater, it can create a story.’”

The iPod was Apple’s first product where Ive applied his design genius to packaging. The result was an elaborate box that cradled the iPod like a piece of jewelry. This packaging was an integral part of the iPod’s success and Apple’s transformation.

Ive and his design team also focused on the insides of a product, normally the responsibility of engineers. When designing the iMac, the original solutions the team came up with pushed the boundaries of traditional manufacturing.

Ive also almost singlehandedly redefined how high-end laptops are manufactured. Kahney explains, “Jony was proud of the PowerBook’s construction, and dismantled one for his 2003 Designer of the Year exhibition at the Design Museum. ‘We took [it] to pieces so you can see our preoccupation with a part of the product that you’ll never see,’ Jony said. ‘I think–I hope–there’s an inherent beauty in the internal architecture of the product and the way we’re fabricating the product: laser-welding different gauges of aluminum together and so on….Jony went on to explain the manufacture of the MacBook Air, Apple’s new razor-thin laptop. Instead of taking multiple sheets of metal and layering them, the new process began with a thick block of metal and, in a reversal of the old process, produced a frame by removing material rather than by adding it. Multiple parts were replaced by just one–hence the name unibody.”

Lessons for iGaming and video game companies

When I started reading Jony Ive: The Genius Behind Apple’s Greatest Products by Leander Kahney, I thought it would be an interesting book with a few tidbits I could apply in the casino space. Instead, almost everything that made Ive, Jobs and Apple great can help both iGaming and social casino companies:

- Simple is better. Most gaming companies focus on adding features and content to grow, while the opposite may generate more success. Look at what you can take out to give the player a better, more directed, experience.

- Play to people’s habits. People do not always act logically. Rather than assuming they will, look at how they actually behave and test different (sometimes illogical) approaches.

- Be bold. Rather than trying to do what everyone else is doing a little bit better (which they are all trying to do), try a new and unique approach.

- Start with the user. Design your product by understanding how your customer will enjoy and use it.

- Attention to detail. Do not settle for good enough, make sure every element, even the smallest, are as great as you can build.

- Encompass everything. Focus on everything, not just the look but the underlying architecture, customer service and all the parts of your product.

If we learn from Ive and Jobs, we can create new and better products despite how competitive the casino space is.

Key takeaways

- Steve Jobs, and his design guru, Jony Ive, turned Apple into one of the world’s most valuable companies because of an unwavering commitment to design.

- Their design philosophy focused on simplicity, the greatest Apple products came from eliminating features and complexity while stream-lining performance.

- Other keys to Apple’s design success are a focus on how the customer will experience the product, not asking customers but understanding customers, making bold decisions rather than evolutionary ones, a focus on detail and including all elements of the product in the design process.

Finding Blue Ocean opportunities in gaming in the post-Covid19 world

Rather than trying to predict when the pandemic will end or the final impact, which is impossible, now is the time to start planning for business opportunities in the aftermath of Coronavirus. I have never been a big fan of predictions, if anyone could predict the future or even trends their income would dwarf Warren Buffet’s, rather it is often an exercise in confirmation bias (remembering our correct predictions) or vanity. A recurring theme, however, of this blog has been the benefits of pursuing Blue Ocean strategy, an approach that has a higher expected return than traditional strategy. While not predicting when the current crisis will end or what the world will look like after it, it is smart to begin planning your economic future.

If you are fortunate enough to experience growth or even stability during the current crisis or are one of the many unfortunate to be furloughed or made redundant during this time, in both scenarios it is important to start preparing your next steps as the world exits the Covid19 situation. A recent article on Forbes, There Will Be Blue Ocean’s Everywhere Post Pandemic by Bob Zukis, reminded me how you should juxtapose Blue Ocean strategy with planning for the aftermath of Covid19. After the pandemic, the often-rare Blue Oceans will be abundant. Anticipating these Blue Oceans and building a strategy to leverage them could result in not only financial stability but big future successes.

Key principles of Blue Ocean Strategy

Before determining how to apply Blue Ocean strategy, it is important to understand the key fundamentals of this approach. First, Blue Ocean is all about turning non-customers into customers, rather than competing for the same customer. By pursuing a Blue Ocean strategy, you create an uncontested market space and make the competition irrelevant. Rather than taking market share, you are creating markets.

Second, developing and implementing a blue ocean strategy involves four crucial actions: eliminate, raise, reduce and create. These are changes to your existing product or a way a market segment is approached. To pursue a Blue Ocean strategy targeting the real money online casino space, for example:

- the first step would be to eliminate. As online players are generally more focused on the underlying gaming mechanic, you might eliminate dealers.

- The next step is raise, that is increase something in the product so it appeals more to this segment. Since casino players are looking for slots, you may launch with 500 different slot machines, more than any land-based casino.

- The third step is to reduce. In this example, since you have a lower cost base, you can probably reduce the amount of each players bet (hold or RTP) that you keep.

- Finally, you need to create, that is add in new functionality for the target audience. If you are creating products for online casino players, maybe you would add in social features that would replace some of the tertiary benefits they get from going to a land-based casino, like a chat function.

If you try to build a Blue Ocean strategy and fail to include these four steps, you will not end up with a true Blue Ocean plan and competitors will quickly eat into any success you experience.

Blue Ocean, gaming and Coronavirus

Covid19 will create an unprecedented plethora of Blue Ocean opportunities, including in the gaming space. Zukis wrote, “rarely do blue oceans appear out of nowhere in business. But they’ll be splashing up everywhere post-pandemic…. When they’ve appeared lately, they can often be more like blue lakes than oceans, and extreme competition from other fishers can quickly turn the lake red.”

You need to understand how the ecosystem will evolve after the pandemic, particularly online. Zukis says, “[the] digital operating system is what will help them find these oceans and navigate the journey safely.” That is, the way people consume and companies deliver content will change. The competitive landscape will also evolve due to the pandemic. While it is impossible to predict the post-pandemic situation, there are several variables to consider and questions to ask when anticipating where the new Blue Oceans will be both for iGaming and social casino (but this can be extended to virtually any space):

- Competition. Many companies may not survive the pandemic. If land based casinos contract significantly, not only would that create land-based opportunities but also may open up other areas that these casinos dominated.

- Regulatory. Will governments, particularly in US states, loosen online gaming regulations to create jobs or generate tax revenue to help pay the huge debt they are building.

- Online collaboration. Will people be more likely to replace business meetings and social get togethers with their virtual equivalents, continuing to use products like Zoom and Houseparty.

- Advertising. With the economic disruption caused by Covid19, the cost of advertising should change (potentially long-term if certain industries do not rebound), new channels will emerge while other channels will disappear.

- Openness to digital Will people, especially older people, be more likely to replace land-based activities with digital content. In the gaming space, will people who previously only would gamble on a physical machine now be open to or even prefer playing digitally.

- Economic situation. Will the world or individual countries rebound quickly or suffer a prolonged downturn. Will the economic shift the importance of certain markets.

- Spend patterns. Will people be more conservative in their spend after the huge economic disruption; as Depression era people always felt a need to keep a strong cash reserve. Conversely, will people spend more easily because they had not spent for months.

- WFH. Companies may decide it is more efficient to let employees continue to work from home or people may decide they prefer WFH than going into an office.

- Investment. Will it be easier to raise funds from VC or Angels, will new investment sources appear or will funds dry up.

- New digital platforms. Will crowd-sourced apps and services like TikTok and HouseParty evolve to become dominant platforms and new ways to reach customers or will new providers like Disney+ and Quibi become the path to reach players.

- Conferences. Rather than visiting conferences, people may prefer to attend virtual conferences. This can lead to fewer conferences or more virtual ones.

- Travel. Will people revert to past travel patterns, travel more to make up for time spent at home or travel less because fears have increased.

- International trade. Will it become easier or harder to operate across borders.

- Commercial real estate. Rents may plummet if retailers are unable to reopen or more companies move to working from home.

By looking at the above variables and then integrating them with the eliminate/raise/reduce/create framework, not only will Blue Ocean opportunities appear but you will appreciate how to pursue them.

Anticipate the competition and move forward

One consideration that is often neglected when building a Blue Ocean Strategy is anticipating the competition and this issue is particularly relevant now. In the post-Covid19 environment, this factor will be even more important as you are not looking for new opportunities in a vacuum; there are hundreds, if not thousands, of other people also thinking about what to do next. They may be forced into the situation because their company has gone out of business or they lost their job or may be looking to accelerate momentum they gained from being in the right place at the right time.

When evaluating your Blue Ocean options, realize that the most obvious ones are likely to be pursued by others. Thus, that beautiful Blue Ocean on your screen may be full of blood before you even get there. That is why it is critical to follow the Blue Ocean framework painstakingly, truly focus on what you can eliminate/raise/reduce/create, and ensure you reach the optimal option. While any new initiative may fail, if you follow this strategy you have the best chance of seeing an outsized return.

Key takeaways

- Blue Ocean strategy historically has a much higher ROI than pursing a Red Ocean approach and Covid19 will create an plethora of Blue Ocean opportunities.

- A Blue Ocean strategy is one where you avoid the competition rather than trying to beat them; you do this by eliminating/raising/reducing/creating features.

- You also need to anticipate what others will do, avoid the obvious as it won’t be a Blue Ocean if five others get there first.

Creating an experience that retains players

One of the most useful book I read last year had nothing to do with tech or the gaming space but was Danny Meyer’s Setting The Table, about how he created an incredibly successful restaurant empire. Meyer, who is not a chef, has built arguably the most successful restaurant business in the hyper-competitive New York market and is one of the founders of Shake Shack. Meyer built his empire not on creative dishes but creating a fantastic customer experience, which resulted in very high customer retention.

Given the importance of retention to game companies, creating a great customer experience is critical to retaining your players. While the product contributes to the experience, there are many other factors. When you go to a restaurant, the food is important but a key reason whether you return (are retained) is the overall experience. You might have great food, but if the waiter is surly, you have an issue paying the bill or even the cloakroom attendant is rude, you might not come back and will probably leave a bad Yelp or TripAdvisor review. Thus, the restaurant industry provides great lessons on how to create a superior customer experience, and Danny Meyer is probably the best restaurateur at delivering a fantastic experience. By extrapolating Meyer’s philosophy into a more general strategy, you can build a roadmap for improving almost any business.

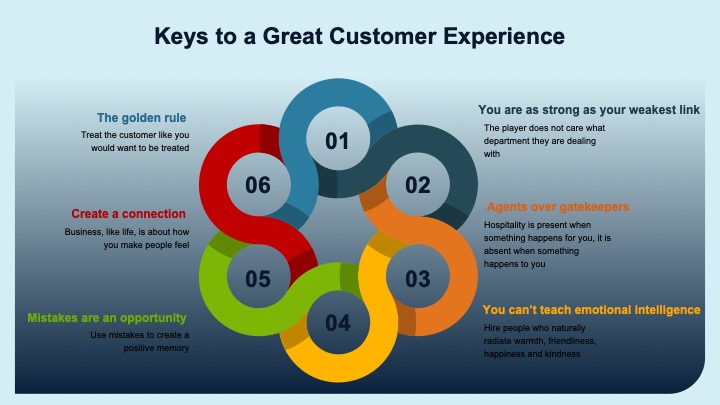

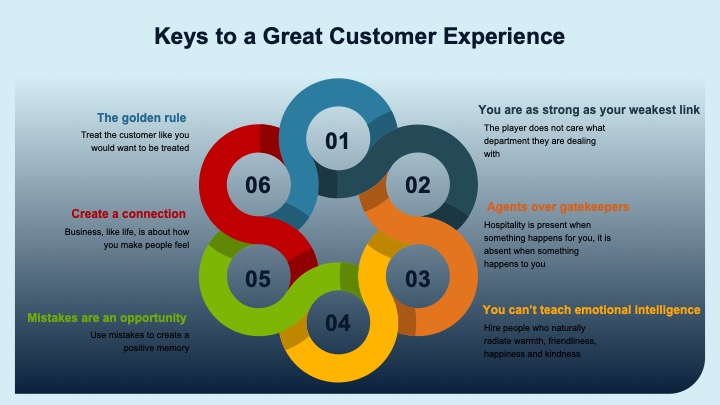

The Golden Rule

Creating a fantastic customer experience begins with the Golden Rule, “do as you would be done by.” In effect, you should treat your customers the way you would want to be treated (and spoken to). If you do not want to get a call at 5 AM, do not try to call your customers at 5 AM because they are more likely to answer. If you would not want to have to answer ten stupid questions to cash out from a casino, do not ask your customer ten stupid questions. In all situations, put yourself in your customer’s perspective and ask how you would want to be approached or treated.

You are as strong as your weakest link

While your core product offering may be fantastic, customers are going to remember the worst part of their experience. If you are in a hotel, you may have a beautiful room with a very comfortable bed but if when you check out you are charged for a bag of cashews from the minibar that you did not take, that is what you are likely to remember. If you go to the hotel restaurant and the food is bad, that is what you will write about on TripAdvisor. It also does not matter to the customer if the restaurant is owned by the hotel or licensed to a third party; the customer will probably be more irate if you try to blame someone else. The key lesson is if you are spending time and money creating a great game or product, do not neglect all the other ways you interact with your customer or player.

Create a connection

One of the strongest motivators for people is seeking connections. As I wrote last week, after satisfying physiological needs and safety, people focus on needs of belonging and esteem, so if the organization is focused on building connections with customers that focus creates tremendous value. Meyer writes, “business, like life, is about how you make people feel….Service without soul is quickly forgotten.” Creating this connection and sense of affiliation builds trust and leads to repeat business.

To create a connection, the first step is to make your players feel important. They should not feel like a number or one of many players (you are number 800 in the queue, please hold on). Every customer should feel like a VIP, they should feel important and loved by the company. According to Meyer, “everyone goes through life with an invisible sign hanging around his or her neck reading, ‘make me feel important.’” If everyone dealing with customers treats them (and considers them) VIPs, you will build a long-lasting connection that keeps the customer from churning and probably improves engagement.

Customer’s time is money

Many companies fail to realize that a customer’s time is more valuable to them than money. All game and gaming companies at their core are entertainment companies, people are choosing between playing your game online or watching the latest episode of the Witcher, land based casinos have learned the Bellagio is competing not only with the Wynn but also with a trip to Hawaii. Your customer facing team must realize it is as important to save customers’ time as how much money they are spending.

Optimizing your customers’ time is also critical in ensuring their experience is better than their next best option. If you are using your customers’ time, you need to provide value (to them, not you) in exchange. Meyer writes, “what mattered most to me was trying to provide maximum value in exchange not just for the guests ’ money but also for their time. Anything that unnecessarily disrupts a guest’s time with his or her companions or disrupts the enjoyment of the meal undermines hospitality.”

If you have a great game, say an online casino, that they enjoy but have to spend half their time dealing with technical issues or trying to cash out, it effectively reduces their enjoyment 50 percent. Even if they get 10 percent more pleasure in your online casino then they would watching the Witcher, by forcing them to waste 50 percent of their time you make the Witcher, your competitor, a superior option.

Agents over gatekeepers

Creating a great customer experiences requires agents to act as advocates of the customers, not as gate-keepers. In every business, there are employees who are the first point of contact with the customers (attendants at airport gates, receptionists at doctors’ offices, bank tellers, executive assistants). Those people can come across either as agents or as gatekeepers. An agent makes things happen for others. A gatekeeper sets up barriers to keep people out. They need to represent the customer’s interest, fight for the customer and thus understand the customer’s concerns. As Meyer writes, “hospitality is present when something happens for you, it is absent when something happens to you.”

Mistakes are an opportunity

To me, mistakes are one of the best things that can happen in the customer experience world. Players remember the way mistakes are handled much more than the mistake and often more than the actual gaming experience. Mistakes provide an opportunity to create a great memory and a connection with your customer. Meyer writes, “The road to success is paved with mistakes well handled. Business is problem solving. As human beings, we are all fallible. You’ve got to welcome the inevitability of mistakes if you want to succeed in the restaurant business — or in any business. It’s critical for us to accept and embrace our ongoing mistakes as opportunities to learn, grow, and profit.”

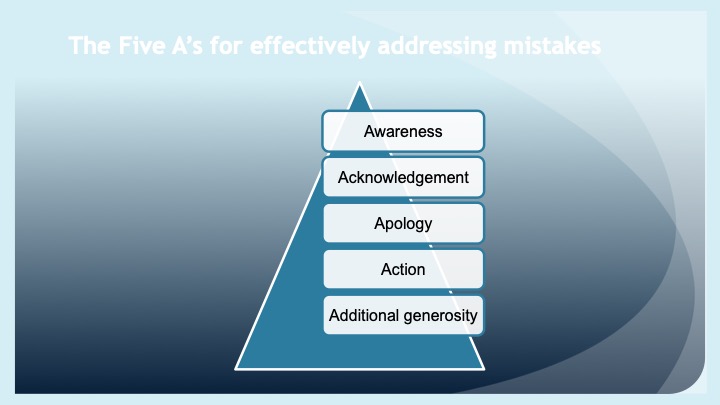

Meyer identifies five elements for effectively addressing mistakes, fortunately all start with the letter A:

- Awareness. Knowing that a mistake has been made.

- Acknowledgment. Admitting that a mistake was made. It is incredibly frustrating having to argue with a company that they made a mistake. I remember a recent business trip to Sydney where the Internet in my room was not working. I had to argue with the front desk, then with a maintenance worker, both assumed that I did not know how to connect my phone to the Internet. Long story short is the wireless access point in the room was broken but their refusal to acknowledge the problem quickly ended up in my cancelling a stay the following month and not staying during visits every quarter. That is the cost of not acknowledging a mistake.

- Apology. Saying you are sorry is an important step in turning a mistake into a good experience for your customer.

- Action. Fix the mistake. Say what you are going to do to make amends then follow through. Make sure that the issue is resolved to the customer’s satisfaction and that you take care of it, do not put the resolution of the problem on the customer (remember to value their time).

- Additional generosity. Do not simply make good for the mistake, provide more than you have to. Turn the bad experience into a great one. If a diner has a bad experience at one of Meyer’s restaurant, not only would they probably not be charged for the meal, but they might get a bottle of wine or champagne.

Another area to leverage mistakes is to turn a customer’s mistake into your mistake. Rather than fighting with a customer, accept responsibility even if it was not your fault. If you stress the customer made a mistake, either they will be mad at you or mad at themselves (if they do not believe you). Either way, they are not having a good experience. Instead, turn the mistake into your mistake and make them happy. That will drive additional engagement.

You need to align hiring with creating a great experience

To create a fantastic experience for your customer or player, the people responsible for dealing with them must have the right mentality. To have the right people, you need to hire the right people. As Meyer stresses, “you can’t teach emotional intelligence.”

You can have scripts and processes for dealing with customers but unless your team members can radiate warmth, friendliness, happiness and kindness, you will not be able to create great experience. Thus, you need to hire warm, empathetic people who have an excellence reflex. The excellence reflex is a natural reaction to fix something that is not right or to improve something that can be better. Not all hiring is perfect, so if you end up with some people who are not empathetic or have an excellence reflex, then you need to find them a new home. Otherwise, you will not be able to create great customer experiences.

You also need to ensure your people can control their moods. We all have bad days, but the customer does not care. You need people with personal mastery, team members aware of their moods and able to keep them in check.

Hiring is the key. As Meyer explained, “Over the years, the most consistent compliment we’ve received and the one I am always proudest to hear, is ‘I love your restaurants and the food is fantastic. But what I really love is how great your people are. ‘ The only way a company can grow, stay true to its soul, and remain consistently successful is to attract, hire, and keep great people.”

Customer experience is the key to success

While it is very challenging to build an organization with great customer experience, it is critical to engaging your players and preventing churn. Meyer’s success using customer experience as the key differentiator in building a restaurant empire in New York City, one of the most competitive and saturated markets, shows how this feature can help companies in other industries (like gaming) stand out and succeed.

Key takeaways

- The key to strong retention is creating a great customer experience outside of the actual product, ensuring that customer contact is extraordinary.

- To create a great experience for customers, everyone dealing with them needs to treat customers as they would want to be treated.

- It is also critical to ensure you have no weak links in your interaction with customers, you create a connection with your player, your people act as agents for the customers and not gatekeepers, you treat mistakes as opportunities and you hire for emotional intelligence.

An often-better alternative to AB testing?

While AB testing is an integral element of mobile and social game development (as well development of most digital products), in many situations there is a better option. Several years ago, I had the opportunity to serve as an advisor to a company that had some brilliant people. Their CTO was a strong advocate of using multi-armed bandit testing as a superior alternative to AB testing. Multi-armed bandit testing is not new, there was a popular post in 2012 (http://stevehanov.ca/blog/index.php?id=132), and it is used by Google and other tech giants, but people (especially product managers) still regularly default to traditional ABn testing.

The problem with AB testing is that you leave money and performance on the table. Until the test is over, the poorer performing variant(s) will always get a significant share of your traffic. With the multi-armed bandit approach, you allocate increasingly less traffic to poorly performing variants.

What is multi-armed bandit testing

A multi-armed bandit approach allows you to dynamically allocate traffic to variations that are performing well while allocating less and less traffic to underperforming variations. Instead of two distinct periods of pure exploration and pure exploitation, bandit tests are adaptive, and simultaneously include exploration and exploitation. As Optimizely wrote recently, ” multi-armed bandit optimizations aim to maximize performance of your primary metric across all your variations. They do this by dynamically re-allocating traffic to whichever variation is currently performing best. This will help you extract as much value as possible from the leading variation during the experiment lifecycle, so you avoid the opportunity cost of showing sub-optimal experiences.”

Multi-armed bandit testing is a Bayesian approach to AB testing. As Shawn Lu writes in a post titled Beyond A/B testing, “The foundation of the multi-armed bandit experiment is Bayesian updating. Each treatment (called “arm”) has a probability of success, which is modeled as a Bernoulli process. The probability of success is unknown, and is modeled by a Beta distribution. As the experiment continues, each arm receives user traffic, and the Beta distribution is updated accordingly.”

A recap on ABn testing

To compare bandit testing with ABn testing (AB is with two variants, a test and control, n allows for additional variables), let’s quickly recap how AB testing works. Alex Atkins summarizes it succinctly, writing “in statistical terms, a/b testing consists of a short period of pure exploration, where you’re randomly assigning equal numbers of users to Version A and Version B. It then jumps into a long period of pure exploitation, where you send 100% of your users to the more successful version of your site.”

Benefits of multi-armed bandit testing

Bandit algorithms try to minimize opportunity costs and regret (the difference between your actual return and the return you would have collected had you deployed the optimal options at every opportunity). Rather than letting an AB test run until it is statistically significant, a bandit test moves subjects into the best performing group faster, allowing you to capture more gains. Matt Gershoff writes, ““Some like to call it earning while learning. You need to both learn in order to figure out what works and what doesn’t, but to earn; you take advantage of what you have learned. This is what I really like about the Bandit way of looking at the problem, it highlights that collecting data has a real cost, in terms of opportunities lost.”

A related advantage of multi-armed bandit testing is you make fewer mistakes. An A/B test will always send a significant portion of traffic to the sub-optimal group.

Also, as Shawn Lu writes, “[an] advantage of bandit experiment is that it terminates earlier than A/B test because it requires much smaller sample. In a two-armed experiment with click-through rate 4% and 5%, traditional A/B testing requires 11,165 in each treatment group at 95% significance level. With 100 users a day, the experiment will take 223 days. In the bandit experiment, however, simulation ended after 31 days, at the above termination criterion.” if the treatment group is clearly superior, we still have to spend lots of traffic on the control group, in order to obtain statistical significance.”

Finally, while not mathematically an advantage, bandit testing relieves the pressure to end a test too early. With ABn testing, frequently you will see one option perform better “directionally” and decide, or be forced to decide, to terminate the test and move everyone to the higher performing bucket before you get significant results. Unfortunately, this sometimes leads to picking an option that would be reversed once there is more data.

Why multi-armed bandit is not always the correct approach

The value of bandit testing does not mean you should abandon completely ABn testing. In Lu’s post, he writes “the convenience of smaller sample size comes at a cost of a larger false positive rate.” That is, you end up sometimes gravitating to the sub-optimal solution.

Alex Atkins also writes, “in essence, there shouldn’t be an ‘a/b testing vs. bandit testing, which is better?’ debate, because it’s comparing apples to oranges. These two methodologies serve two different needs.”

A/B testing is a better option when the company has large enough user base, when it’s important to control for type I error (false positives), and when there are few enough variants that we can test each one of them against the control group one at a time.”

The Bandit Option

While multi-armed bandit testing is not always a better option than ABn testing, you should look closely at using bandit testing when possible. It can reduce the opportunity cost of your testing and relieve pressure to terminate tests prematurely.

Key takeaways

- While AB testing is the most common method of optimizing between alternatives, in many situations the multi-armed bandit approach is optimal.

- A multi-armed bandit approach allows you to dynamically allocate traffic to variations that are performing well while allocating less and less traffic to underperforming variations.

- Multi-armed bandit testing reduces regret (the loss pursing multiple options rather than the best option), is faster and lowers the risk of pressure to end the test prematurely.

Recruiting Live Services Product Manager

I am recruiting an experienced Product Manager, preferably from the social casino space, to join my Live Services team to grow further our Chumba Casino revenue (up over 20 percent this year, so far). We are open to locating the Product Manager at our Toronto, Malta, Perth or Syndey office, and would relocate a great person. Feel free to apply online or email me directly.

Lifetime Value Part 28: Why you are probably under allocating resources to Live Services

Last month, I wrote a post about how many game companies do not dedicate enough resources to retention. Another area that most game companies, other than the top mobile gaming companies, are also under allocate resources to is live services. The live services team, however, largely drives success in the gaming space. A strong live services team is a key part to having an LTV that justifies marketing (and thus growth).

During the MAU conference in April, there was an interesting session on why the top social casinos were successful. The speakers were from the leading social casino publishers, Playtika, Zynga and Play Studios. All of them credited live services as the key to their success, with one attributing 80 percent of their success to live services. Also, if you look at the recent surge in Zynga’s stock price, it is largely driven by the performance of recent acquisitions. Zynga’s ability to improve the live services at these studios is the key driver of this positive performance.

What are live services

The textbook description of live services are changes that are made to a game or app that do not require a new build (development work). Live services product managers are focused on optimizing retention or monetization KPIs, rather than the PMs or designers driving new content or features.

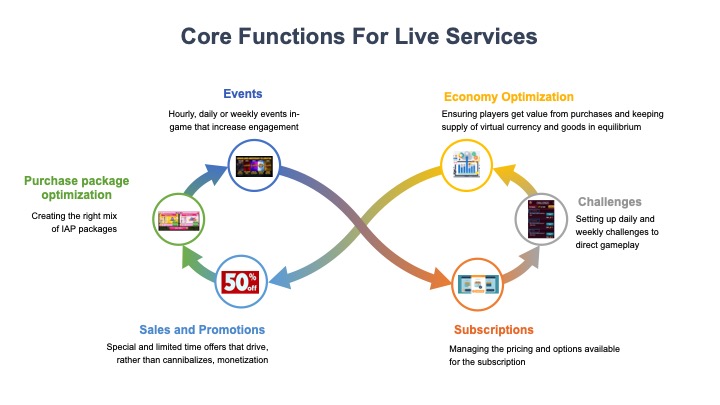

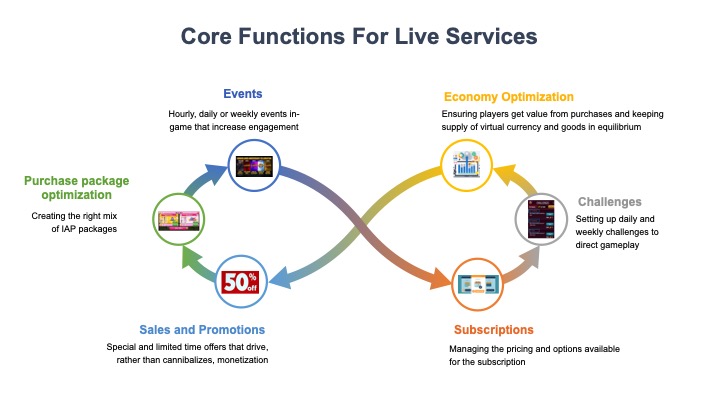

There are many types of live services initiatives, ranging from optimizations to full programs. Some that have strong impact include:

- In-game events. In many mobile games, you will see daily or weekly (sometimes hourly) special events, such as a one-day race to the top. The event may include a special leaderboard for players who get the most combinations or kill the most of a certain type of enemy in a specified period. These events serve multiple purposes. They create a sense of excitement outside the core game loop. They provide a reason for players to replay a level or a machine. They drive more engagement as players compete to get higher on a leaderboard. They provide variation, a way of introducing new content without having to build more content. Events are one of the strongest drivers of both retention and monetization KPIs in the gaming space.

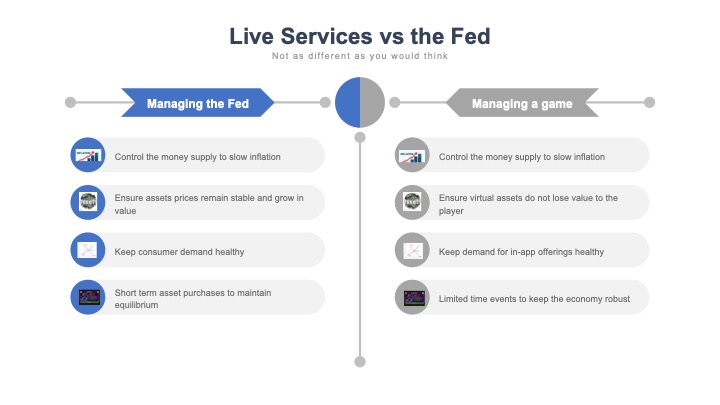

- Economy optimization. A key to keeping a free-to-play game successful long-term is managing the economy, an incredibly complex task. Managing the economy of a social game (or real money poker) is very similar to what Jay Powell, Chair of the Federal Reserve or Mark Carney, Governor of the Bank of England, must manage. Powell and Carney must regularly adjust interest rates, quantitative easing (asset purchases), reserve requirements, borrowing levels, etc. to manage inflation, demand, unemployment and the asset (stock) markets. If Powell or Carney gets it wrong, inflation could get out of control, unemployment could rise or asset prices (stocks and real estate) could plummet.

It is the same in games. The Live Services team must ensure that the in-game economy stays in sync and is a good experience for all players while encouraging spend (keeping up the value of assets). They need to ensure prices for goods or bets in a casino are at a price level that gives players a fair return on their investment and keeps them engaged. They need to build a balance between the main and premium currencies. They need to ensure the spin speed of a slot creates a good experience without draining a player’s wallet. They need to guarantee that a new player has a good experience but elder players are still having fun. All of these initiatives are connected and a failure in one area could create the gaming equivalent of Venezuela.

- Purchase package optimization. Related to optimizing the economy, the live services tem must ensure continuously players are getting appropriate value for their purchases. If packages are priced incorrectly, a customer might not get sufficient value when they make a purchase (for example, five minutes of gameplay rather than one hour) and thus become less likely to make future purchases. Conversely, they may get so much value that they never have a need to make additional purchases.

- Challenges. One of the most engaging features in games are challenges. Challenges are usually offered on a daily or weekly basis, helping direct gameplay. They are useful for keeping players engaged, encouraging them to test new content or features or play more. The live services team should create effective challenges and structure them (rewards, timing, amount of effort required, etc.) to optimize the impact on KPIs.

- Sales and promotions. Just as in the retail space, sales and promotions are a valuable driver of monetization. If not structured properly by the live services team, the sales could end up cannibalizing purchases or negatively impacting the economy. When done well, they encourage higher sustained revenue.

- Subscriptions As I have written recently, subscriptions are a great opportunity for game companies. Managing the pricing and options available for the subscription model sits with the live services team.

This list is a subset of some of the projects that are driven by a good live services team. Strong live services product managers will proactively identify other areas of optimization that will improve retention and monetization.

While I previously said that the live services team drives improvements that do not require development work, that is often the case in theory only. Many games are not architectured in a way that these changes can be made without development, especially older products. The need for development work should not be a line in the sand on whether these initiatives are pursued by the live services team, the benefits of launching events or optimizing the economy persist regardless of any need for development. Additionally, most successful live services teams also impact the product development efforts, for example ensuring the pricing of a new feature enhances the existing product.

Where’s the love

Just like it’s cousin retention marketing, many companies do not allocate sufficient resources (financial and people) to live services. Most of the resources end up going to product development instead. This allocation occurs because the development side is on the face of it easier to measure and sexier. A new feature under development might have a projected impact of a 2% lift on revenue after six months of development. That 2 percent uplift would be incorporated in the financial projections and when the feature launches and the revenue accelerates, everyone is taken to dinner. The PM who designed the feature can then create a Powerpoint that they use to brag to their colleagues.

Live services is not as glamorous. Economy improvements might improve revenue 0.5% every month but over the course of the month, not overnight. The live services PM probably won’t be taken out to dinner for the 0.5% increase (especially as it does not happen overnight but gradually over the month) over a given month. Over the same six months that it took to develop the larger feature, however, the economy improvements generate over 3 percent uplift (assuming the improvement is compounded monthly), a 50 percent larger increase than the new feature. Additionally, it does not require the development resources (and costs) that the new feature absorbed.

The other factor inhibiting allocation of sufficient resources to live services is the cross over with marketing. Many of the live services activities described above fall under marketing at some game companies. As marketing is often focused on acquisition, it is not prioritized on the marketing team’s agenda. Even when it is, live services need to be integrated with the core game experience to succeed. The expertise to design and optimize live services is usually more consistent with Product Managers than Marketing Managers.

Live services is critical to managing your LTV

I have written many times about lifetime value (LTV), and as I have said before it is the lifeblood of any app or game. Products are successful when their LTV is greater than the cost of acquiring a new user (CPI), only when this happens can a company afford to market. Without marketing, products eventually wither and die. Most companies, particularly in the social gaming space, are fighting a perpetual battle to find acquisition channels where LTV is great than CPI. Live services drives continuous improvement of LTV, thus allowing products that would otherwise not justify acquisition thrive. It is often the big difference between the game companies that can maintain their franchises (see Words with Friends, Slotomania, Clash of Clans, etc) to the ones that rise and then burn out.

Key takeaways

- Live services is the key to the success of the largest mobile game companies (Supercell, Zynga, etc.) but it is an area often over under resourced at other companies.

- Live services projects include in-game events, economy and purchase package optimization, sales, challenges and subscriptions.

- Live services often get fewer resources than product development because a new feature that takes six months to develop and generates a two percent revenue uplift is sexier and easier to visualize (and put in a P&L) than improvements that add 0.5 percent a month, though the latter leads to a 50 percent bigger impact.

Why iGaming is not doomed, but doomed to be like the airline industry

Last week, a post on LinkedIn that the iGaming (real money online gambling) industry is in trouble gained traction but the article missed the reality of the iGaming space. Rather than doing poorly, the industry is becoming normal. In many ways, it is following the evolution pattern of the airline industry, which grew from a highly profitable business that succeeded largely due to regulation and barriers to entry to a very challenging business where only good companies do well.

Trouble is a relative term

Rather than being “in trouble,” the iGaming industry is suffering from unrealistic expectations. William Hill, an iGaming stalwart that was called out in the post, for the first half of 2019 had online revenue of over $425 million. While they do not report EBITDA, a similar metric would have shown an EBITDA profit of about $285 million.

The Stars Group, another industry behemoth, has seen its stock price hammered in the past year, announced EBITDA (earnings before taxes, interest and depreciation) of over $236 million and a margin of 37.1% last quarter. If you annualize that profit (EBITDA), it suggests earnings of nearly $1 billion. The performance of the other top gaming companies (Paddy Power, GVC, etc.) is in line with Stars and William Hill.

The numbers above show that iGaming companies are not hemorrhaging cash or on the verge of bankruptcy. They are still profitable large entertainment companies. They are not going away. There are very few companies in the world that would not take $1 billion in profit and a 37% margin.

So why is the iGaming business described as in trouble? Why are the share prices of most of the companies near 1-year and 3-year lows? Why are CEOs getting replaced faster than Tom Brady throwing touchdowns?

The negative sentiment is driven by high expectations, excessive debt, bad habits and a new business environment. The sentiment is also realistic, it reflects the reality that iGaming companies face, particularly the legacy operators.

The high expectations game

The great numbers put up by iGaming firms since the first companies went live created multiple problems for the industry.

- Expectations beget expectations. The more the industry, and particular companies, grew, the more analysts and investors expected them to grow. The growth rates were much higher than other industries. Over time, growth is likely to revert to the average growth rate for all industries (reversion to the mean). Not only does this reversion disappoint investors but it also prompts the actors in the industry to make non-judicious decisions to chase unrealistic profit and revenue targets.

- High margins drive competition. The core of capitalism is that capital flows to where it will have the biggest return. Capitalism creates an efficient allocation of resources. When there are “excessive profits” (an economic term referring to profit levels above the average for other industries), capital will flow to that industry, either financing new entrants or providing growth financing for existing companies. Capital will flow in until this expansion of supply drives down margins to “normal” levels. This phenomenon is shown by the hundreds of slots providers that are visible when walking around ICE or any gaming conference.

- High expectations creates high debt. High expectations are not limited to investors. Companies themselves believe the growth will never slow. They then use this expected growth to project cash flow that justifies acquisitions (for example, GVC’s acquisition of Ladbroke Coral). When the growth fails to materialize, financing the cost of the acquisitions becomes a challenge.

When the reality does not meet expectations, particularly if the expectations do not shift, successful companies will be disappointing. Owners and investors will drive leadership changes, strategies will shift and new initiatives will begin often in an effort to actualize a future that will never exist.

It was too easy, too long

Another challenge facing the iGaming industry is that it has been too easy for too long. I had the luck of being in both the social and real money gaming spaces. One of the glaring differences is that for many years in real money gaming, particularly real money casino, it was very easy to make money. An operator could add slots to a website or launch a new app (they did not even have to build the slots as there are many providers with a huge catalog) and the more users they drove, the more money they made. The products were largely undifferentiated (in part as everyone licensed the same content) but the more that was spent on marketing, the more money companies made. Also, despite robust affiliate fees and seemingly high CPAs, it was relatively easy to grow products in a profitable way (unlike social casino where margins are wafer thin).

The ease of building a successful real money gaming company led to the high expectations detailed above. It also allowed companies to thrive without creating very compelling products. If you compare the user experiences of most iGaming apps, they are often years behind other entertainment or app offerings. Rather than optimizing the on-boarding funnel or building engagement loops to retain players, many Real Money gaming sites are little more than glorified spreadsheets. As consumers’ expectations continue to grow, this delta between expectations and what iGaming companies deliver helps drive the “troubles”.

The good times of the past have also allowed iGaming companies to stay in the past. It is probably the only industry that still talks about “mobile first.” Mobile is so integrated into virtually every other facet of our lives that even having to acknowledge that mobile is a priority highlights how far behind other industries iGaming has fallen.

What is next for iGaming

iGaming is evolving in a pattern similar to how the civil aviation industry developed. For many years, airlines and suppliers enjoyed very high profit levels as they were in a regulated industry. These companies grew into huge worldwide brands. While there were a few failures from the worst managed, it was a very stable business.

This stability led to an industry that diverged from its customers as it did not have to please them daily to survive. When the industry deregulated, these companies could not become customer friendly. They just did not understand their customers or have the right management in place. The airline industry still has one of the lowest levels of satisfaction of any consumer facing business.

They also went on a spate of mergers and acquisitions because of high expectations, creating debt service burdens that bankrupted many airlines (including huge global brands). The industry also experienced many challenger brands (Southwest, EasyJet, RyanAir, etc.) entering the market who displaced the legacy airlines.

While the iGaming industry is going in the opposite direction with regulation, it is following the path from where a few companies generated “excessive” profits to one with high levels of competition. It is also one where most of the legacy companies are not customer centric. Based on the lessons from airlines, we should not expect these legacy companies to improve their offering significantly (anyone fly BA lately), many of them will not survive including some of the largest (remember Pan Am) and industry profits will settle into much more normal numbers with some winners and some losers.

Key takeaways

- There is significant negative sentiment around the iGaming industry, including depressed stock prices and frequent leadership changes. The reality is that the industry is still healthy with many companies enjoying solid revenue and strong margins, but the growth is not living up to expectations.

- The industry is in this situation as the high growth and profits in the past led to unrealistic expectations that have driven more competitors and more debt and allowed companies to flourish despite products that are not centered around their customers.

- Many of these legacy companies will fail to improve their offering significantly, many will not survive and industry profits will settle into normal multiples and growth rates.

Subscriptions: The new weapon in the game monetization arsenal

People in the game industry are continually asking about “a new business model” but they usually want new monetization techniques (ie. gatcha mechanic, piggy bank, etc.). Now, however, there is a real opportunity to disrupt the industry with a new model, subscriptions. I have been in the games industry since 1993 and in that time there have only been two new models, try-before-you-buy and free-to-play. Subscriptions may usher in the next era of gaming.

Try-before-you-buy was introduced in the early 2000s and perfected by Big Fish Games, who released via download a game every day that was free for the first hour and then the player would have the option of purchasing the full game. While the model did not have a huge impact on the traditional game companies (who were selling their product for a fixed cost in retail), it was blue ocean as it brought an entirely new demographic into gaming. For the first time, gaming was not dominated by teen age boys playing in their parents’ basements (or 30 year old boys playing in their parents’ basements) but saw an influx of female players, particularly older women.

Early in the 2010s the gaming industry experienced its greatest disruption. Free-to-play gaming gained traction in the US (and Europe) after dominating Asian markets. In this model, games were truly free and over 90 percent of the players would never spend a penny. The games, however, were built to get the most engaged players to spend to improve or speed up their gaming experience, and many of these players would spend tens or even hundreds of thousands of dollars in their favorite games. Social gaming companies, led by Zynga, gained millions of daily players, pulling them from other gaming or entertainment companies.

Free-to-play was truly disruptive. Household names like Atari, Acclaim and THQ (which had earlier reached over $1 billion in sales) went bankrupt. Zynga saw its valuation reach over $10 billion. Disney and Electronic Arts both spent hundreds of thousands of dollars to acquire companies in the space. The concepts behind free-to-play have grown to shape the video game space, even those old-school companies that still monetize with an upfront purchase use in-game monetization to drive their revenue growth.

Given the impact of free-to-play and the millionaires it, everyone has been looking for the next disruptive business model. Based on how other industries are evolving, subscriptions are likely to be the next disruptive model in the game industry,

How subscriptions are changing the world

While Asia provided a clue that free-to-play would disrupt Western video game markets, developments in other industries show the likelihood that subscriptions will emerge as a disruptive force. The largest retailer in the world (by market cap), Amazon, uses its Prime subscription service to lock in customers. Salesforce.com, the most important company in the enterprise software space, eschewed the high fixed fee model for a subscription model that left its established competitors in the dust. Adobe, the largest provider of graphics software, abandoned its old business model to move to a subscription model and is now valued at $135 billion. Netflix, the second most important entertainment company in the world (nobody is beating Disney for a while), gained its position with a subscription model. Even Disney is betting its future on subscriptions with Disney Plus.

Enabling this shift is a change in people’s attitude. Ten years ago, people would not pay for digital content and overall wanted to own things. People did not pay for music (remember Napster). People would buy a DVD or CD, even if they would only experience it once. The examples above (and the hundreds I left out) show that attitudes have shifted. Millions of people are willing to pay Spotify money every month without owning a song. According to the Reuters Institute, in the United States, the proportion of people ages eighteen to twenty-four paying for online news leaped from 4 percent in 2016 to 18 percent in 2017. Attitudes have clearly shifted.

Why subscriptions work

Subscriptions have succeeded because they better align customers with providers than other business models. Rather than the linear model of selling a product to a customer, the subscription model creates a dynamic where the company to please constantly its customers. As Tien Tzuo says in Subscribed, “companies that know what their customers want, and how they want it, will succeed over companies that spend a lot of time and effort creating a product they think is a good idea, then spend equal amounts of time and effort trying to persuade people to buy it.”

Further driving the success of the subscription model are the benefits it has for the provider. Subscriptions allow companies to start the month (or year) with a guaranteed base of business. Rather than having to estimate how many units you will sell, you look at your subscriber base and can accurately forecast your revenue. This stability allows companies to market aggressively, invest in new content, etc., as they can predict cash flow.

The subscription model also aligns companies with their customers. As Tzuo writes, “instead of thinking about reseller margins and unit sales, [companies are] thinking about subscriber bases and engagement rates.” Companies driven by a subscription model have direct ongoing relationships with their customers. They no longer have to segment customers, they now have individual subscribers. With the industry leaders (Amazon, Netflix, etc), every subscriber has their own home page, their own activity history, their own red flags, their own algorithmically derived suggestions, their own unique experiences. And thanks to subscriber IDs, all the boring transactional point-of-sale processes disappeared. As companies can never be too close to their customers, subscriptions create the loop that makes customer intimacy a reality.

Will subscriptions work in the game industry

Now that we agree that subscriptions are a great opportunity overall, will they work in the game industry. First, many game companies already are using this model. According to a great blog post by Google, they have seen global growth in game subscriptions of 70 percent year over year. Second, it is working. According to the post, game companies that have integrated subscriptions experience 20 percent higher retention. They also have seen higher overall monetization. Finally, subscriptions offset risk in developing and launching new content. According to Tzuo, “regardless of whether a show is successful or not, investing in sharp new content helps Netflix to both (a) attract new subscribers and (b) extend the lifetime of its current subscribers. Those shows don’t go away! Together, they’re increasing the overall value of the portfolio. They are instrumental in driving down customer acquisition costs (as more subscribers sign up) and increasing subscriber lifetime value (as more subscribers stick around for longer).”

How you should implement subscriptions in games

While subscriptions are an exciting opportunity, success with the model will come down to execution. Just as hundreds (or thousands) of game companies failed to implement successfully free-to-play, succeeding with subscriptions is more difficult than adding another package to your purchase page. There are several core concepts in building a product that leverages subscriptions.

Subscriptions need to be about access

The biggest challenge, and most common mistake, game companies face is what to provide for the subscription fee. The easy answer is virtual currency, after all it is what customers are willing to pay for with in-app purchases. The easy answer is wrong. As stated in the Google post, “it’s important to move away from the mindset that subscriptions are just an auto-renewal mechanism for discounted IAP. Instead, subscriptions need to be thought of as offering highly-retentive long-term access to content, rather than the one-time situational purchase of content offered by IAP.”

Successful subscriptions are about giving players access to content and special benefits, access that can be gained or lost. In a social casino, it could be access to new slots or unique table games. In a game like Archero, it could be access to special levels or powers. The benefits could also be exclusive tournaments, special avatars or unique in-game events. The key, though, is not limiting (or even relying) on giving players virtual or premium currency but access to a premium experience.

Keep it simple

One of the core principles in creating successful products is to focus on simplicity, which is often very complex to do, and subscriptions are one area where it is easy to fall into the complexity trap. Companies with very successful subscription offerings have very few options.

If you offer customers too many options, it is likely to overwhelm them and preclude them from choosing any of the options. This concept of cognitive load is critical to the success of many products, from games like slots to apps like Uber. Given that the human brain consumers 20 percent of the body’s energy but only is 2 percent of the body’s mass, it is important to understand that people will subconsciously work to reduce the amount of energy the brain is using.

Cognitive load is how much info people are processing at any one time. Cognitive load is tied to working memory, the more information in that short-term memory the higher the cognitive load. As cognitive load increases, consumers are less likely to make a purchasing decision.

With subscriptions, this is directly tied to the offerings. If a player has different options ranging from the term of the subscription, monthly costs, benefits levels, they are likely to choose none. For example, you might offer people a month-to-month, 3-month-, 6-month or 1-year plan, with pricing at $4.99, $9.99, $19.99 and $49.99, each with different benefits. Rather than the player finding the one that optimizes their utility (to use an economist term, or makes them happiest, to use a human term), they are more likely to shut off and just pass on the offerings.

Instead, offer them one or two (at most) options. It can be a regular subscription or a premium one (additional benefits) or a short-term plan and an annual plan. You do not see Netflix offering ten different types of subscriptions. The key is make it very easy for the player to understand the value and choose between the two plans and whether or not to subscribe.

Keep it honest

One of the reasons subscriptions took so long to be commonly accepted is that until recently they were part of a sleazy industry. Companies would trick customers into signing up for a subscription, then make it very difficult to cancel the subscription. They might let you sign up easily, then require you to call them to cancel at a call center open one hour a week every second week. Even then, the agent you spoke to would do everything humanly possible to keep you from cancelling, creating an awful experience. These practices soured people overall on signing up for subscriptions. With social media and sites like TrustPilot, word quickly gets out of deceptive subscription tactics.

Preventing customers from leaving or tricking them into subscribing is not only unethical, it is bad business. One of the fundamental values that subscriptions create for a business is the connection with the customer. It forces the company to ensure every month it is creating value for the customer and that is why the customer renews or maintains the subscription. Everyone on the product team looks at new content and features and judges whether it will help retain customers and bring in new subscribers. While scamming customers may bring short term gain, it is the customer connection that subscriptions create that leads to great companies like Amazon, Netflix, Spotify, etc.

The best companies use subscriptions to improve their underlying business. Tien Tzuo writes in Subscribed that “the smart [companies] realize that if they really want to retain their subscribers, they need to focus on building a great service, without relying on lame tricks like hiding the cancel button.…Make it easy for customers to leave if they want to. You can certainly ask them why they’re leaving, or try to win them back, but don’t get in their way—the digital equivalent of blocking the exit with a hulking security guard. When you build subscriptions into your game, let customer value drive the offering rather than tricks on keeping customers from cancelling.

Build a loop

A successful subscription plan should be tied to engagement in the underlying game. The more a customer plays the game, the higher the value of the subscription. According to the Google post, “in mobile games’ subscriptions design, some offer a booster or bonus points, to reinforce the action of ‘play.’ Some create a durable good, such as a permanent building or character, that levels up as a player remains a subscriber for a longer period of time. In these cases, the desired action is “continue to subscribe.” In other cases, subscribers get bonus premium items, currency or points to reinforce the action of in-app purchases.

Looking outside the game industry, airlines have done a good job of creating a loop around their frequent flier programs. With frequent flier programs, members improve their status by flying more or buying expensive tickets, such as business class. According to the Google post, “the ‘earn’ criteria here — flying or spending — is precisely the desired customer actions that the airlines want to reinforce.”

Evolve benefits

Another important element of a successful subscription program is that benefits evolve. According to Google, “as the players invest more in the game, whether it’s with their time, skills, or other IAP, the subscription benefit also compounds.” Thus, the player can unlock more sophisticated content or new challenges that would not have been relevant for them earlier in their experience.

Celebrate VIPs

VIPs are the core of virtually any social game’s success. Most free-to-play games generate 60-90 percent of their revenue from the top 1 or 2 percent of players. Many product managers have avoided subscription programs because of concern on how it would impact VIPs. If a player can subscribe to a VIP program for a fixed sum, the concern is that would put a cap on how much the VIP would spend in the game.

This concern leads back to the first point on subscription design, that is should be about access, not a replacement for existing purchases. Thus, the subscription plan might give the VIP access to slots they would love to play but not chips to play those slots.

When thinking about your VIPs, do not forget they are already VIPs. If someone is spending significantly in your game, do not try to take another $5 or $10 from them every month. Instead, turn the subscription into a celebration of their VIP status. Give them a free subscription, the goodwill will be worth much more than the short term revenue you would generate from forcing your VIP to purchase a subscription.

Use subscriptions to drive acquisition and convert players

In addition to driving monetization and engagement, subscriptions are a great way of increasing retention they are also a strong acquisition tool and powerful CRM element early in the product life cycle. First, an offer of a one or three month complimentary subscription can entice a potential customer not only to try your game but invest time to learn about your product.

Second, subscriptions can help convert players into customers of in-app purchases. They provide a way to let players see and test the spectrum of in-app offerings. According to Google, “Scopely’s game Wheel of Fortune frames its subscriptions offer as an all-access pass. These subscriptions feature exclusive rewards that a potential buyer would want in addition to a sales discount. Surfaced right after the first-time user experience (FTUE), with benefits such as ‘more energy, this subscription aims to increase these new buyers’ in-game engagement, and cultivate a habit of playing regularly and investing in their future gameplay.”

Third, subscriptions can increase virality, helping your existing users bring in new customers. Campaigns that let your subscribers give free months to their friends, and get free months themselves, are very effective at driving new user acquisition. For example, a promotion where a player can gift a new player three free months, and get a free month for every new player who signs up, helps you acquire players with the only cost being the lost subscription revenue of your advocate.

Making subscriptions a reality